If you want crypto to feel spendable instead of stressful, stablecoins usually beat BTC and ETH. Bitcoin changed money. Ethereum changed what money can do. But when you actually want crypto to behave like money in daily life, stablecoins are usually the asset that makes the most sense.

TL;DR

Stablecoins are becoming the default payment asset in crypto because payments need predictability more than upside.

Bitcoin is better suited to long-term value storage, Ethereum is better suited to powering apps and onchain activity, and stablecoins are better suited to behaving like spendable money.

That does not make them risk-free. It just makes them a better fit for the job. When the goal is practical movement of value, stability and wallet experience matter most.

Stablecoins are usually the best crypto asset for everyday spending because they hold a steadier value than BTC or ETH while still moving on blockchain rails. Bitcoin makes more sense as a savings-like asset, Ethereum makes more sense as programmable infrastructure, and stablecoins make more sense when you need money to stay legible from one transaction to the next.

Related: Can You Pay With Crypto in Everyday Life?

There is a reason this question keeps coming up. People do not just want crypto that can go up. They want crypto they can actually use. They want to send money, hold value between transactions, pay someone, move across borders, or stay in dollars without going back through a bank every time. That is where the difference between BTC, ETH, and stablecoins stops being theoretical and starts feeling very practical.

And this is exactly where walllet.com becomes relevant. walllet.com is a non-custodial smart Web3 wallet with hardware-level security that supports crypto and stablecoins across major chains. Its current product language leans hard into one simple promise: make crypto feel easier to use, not harder to survive. That framing fits this topic almost perfectly.

Asset | Best fit | Why people use it | What makes it awkward for everyday spending? | Practical takeaway |

Stablecoins | Payments, transfers, holding a digital dollar or euro-like balance | Stable value, easier pricing, simpler mental model | Issuer risk, depegs, chain confusion, wallet friction | Usually the best fit when you want crypto to act like money |

Bitcoin (BTC) | Long-term holding, reserve asset, censorship-resistant savings | Scarcity, decentralization, strong store-of-value narrative | Price swings make routine spending harder to predict | Better for holding than for day-to-day pricing |

Ethereum (ETH) | Onchain activity, smart contracts, DeFi, network fees | Powers apps, tokens, and settlements across Ethereum ecosystems | Volatility plus gas role make it awkward as a spending unit | Essential infrastructure, but not the cleanest day-to-day payment asset |

That table is the short version. The deeper answer comes down to one question: what do you need the asset to do? If the answer is “hold long-term value,” BTC has a strong case. If the answer is “use apps, pay gas, interact onchain,” ETH matters. If the answer is “send $50 and still have it feel like $50 when it lands,” stablecoins usually win.

Why volatility is the enemy of everyday payments

Payments are not supposed to feel like a trade.

That sounds obvious, but crypto often forgets it. When you spend BTC or ETH, you are using an asset whose price can move meaningfully over short periods. That is fine if your main goal is exposure, upside, or participation in a network. It is not so fine if your goal is dinner, payroll, rent, or sending money to someone who just wants the amount to arrive intact in meaning, not only in units. Stablecoins are designed for payments and differ from volatile cryptoassets because their value is linked to a reference asset, usually a fiat currency.

Related: Best Crypto Wallet for Beginners: What to Look for Before You Download Anything

This is why stablecoins feel more natural for payment behavior. They preserve the part people actually need from money in daily life: a stable unit of account. Stablecoins can be described as digital assets designed to hold a steady value so businesses and individuals can treat them more like digital cash. That alone changes the user experience. You can price something. You can compare values. You can send a balance without wondering whether the asset itself changed character overnight.

Bitcoin and Ethereum are both hugely important. They are just doing different jobs. Bitcoin primarily can be described as a store of value and Ethereum as programmable infrastructure that powers smart contracts and decentralized apps. Those are strong roles. They are just not the same as “default payment asset.”

Why are stablecoins better for payments?

The first reason is stable value.

A payment asset works best when its meaning is predictable. If you send 100 units, both sides want those 100 units to map cleanly to a real-world value. Stablecoins were built for that. Fiat-backed stablecoins are typically backed 1:1 by cash or cash equivalents such as short-term Treasuries, which is why they have become the most common type for payments.

Related: Stablecoins 101: USDC vs USDT vs DAI

The second reason is settlement speed and availability.

Stablecoins keep the always-on nature of blockchain rails. Stablecoin transfers can settle in minutes, at any time of day, anywhere and stablecoin-based payments are typically near-instant, lower-cost, traceable onchain, and available around the clock. If you have ever dealt with payment cutoffs, weekend delays, or international transfer friction, you can see why this is attractive.

The third reason is mental simplicity.

This part gets underrated. People do not only need technical speed. They need a clear mental model. Stablecoins are easier to reason about than volatile assets. A dollar-pegged balance feels closer to familiar money behavior. That does not make it identical to bank money, and it does not remove risk, but it lowers the cognitive friction. For many users, that is the difference between “crypto is possible” and “crypto is usable.”

The fourth reason is that the payment use case is becoming more credible, even if it is not fully dominant yet.

The nuance matters here. Most stablecoin turnover still relates to crypto trading today, but cross-border payment flows are growing quickly. Trading is still the dominant use case, yet cross-border payments are frequently cited and regulatory clarity is expanding across major jurisdictions. So the story is not “stablecoins have already replaced everything.” The real story is more interesting:

They are increasingly the asset people reach for when they want crypto to behave less like speculation and more like money.

Are stablecoins safer to spend than BTC or ETH?

For payment predictability, yes. For total risk, not automatically.

That distinction matters. Stablecoins are safer for spending in the sense that they reduce price volatility risk. If you pay with BTC or ETH, you are spending a moving asset. If you pay with a well-established fiat-backed stablecoin, you are spending something designed to stay close to a reference value. That usually makes budgeting, pricing, and transfer expectations cleaner.

But stablecoins introduce a different risk stack. The peg can wobble. Redemption confidence can break. The issuer matters. The reserves matter. The chain matters. The ECB warns directly about de-pegging and runs, while the IMF notes that stablecoin values can fluctuate if users lose confidence in the ability to cash out.

The safest way to think about stablecoins is not “risk removed.” It is “risk changed.”

That means the useful comparison is not “stablecoins are perfectly safe, BTC and ETH are dangerous.” The better comparison is this: stablecoins are usually better suited to the job of spending, while BTC and ETH are usually better suited to different jobs.

Where stablecoins still create risk or friction

A stablecoin can still fail you in four common ways.

First, the issuer and reserve model can become the problem. Payment stablecoins depend on trust in the backing, the redemption path, and the operating structure behind them. That is why reserve quality and transparency matter so much. The Federal Reserve note stresses backing by relatively safe assets, and Stripe recommends choosing stablecoins based on issuer transparency, reserve quality, liquidity, and regulatory posture.

Second, the peg can slip. That is what de-pegging means. The ECB and Bank of England both make this point in different ways: stability is the goal, not an absolute guarantee. If confidence drops or redemption pressure spikes, a supposedly stable asset can start behaving less like cash and more like a stress test.

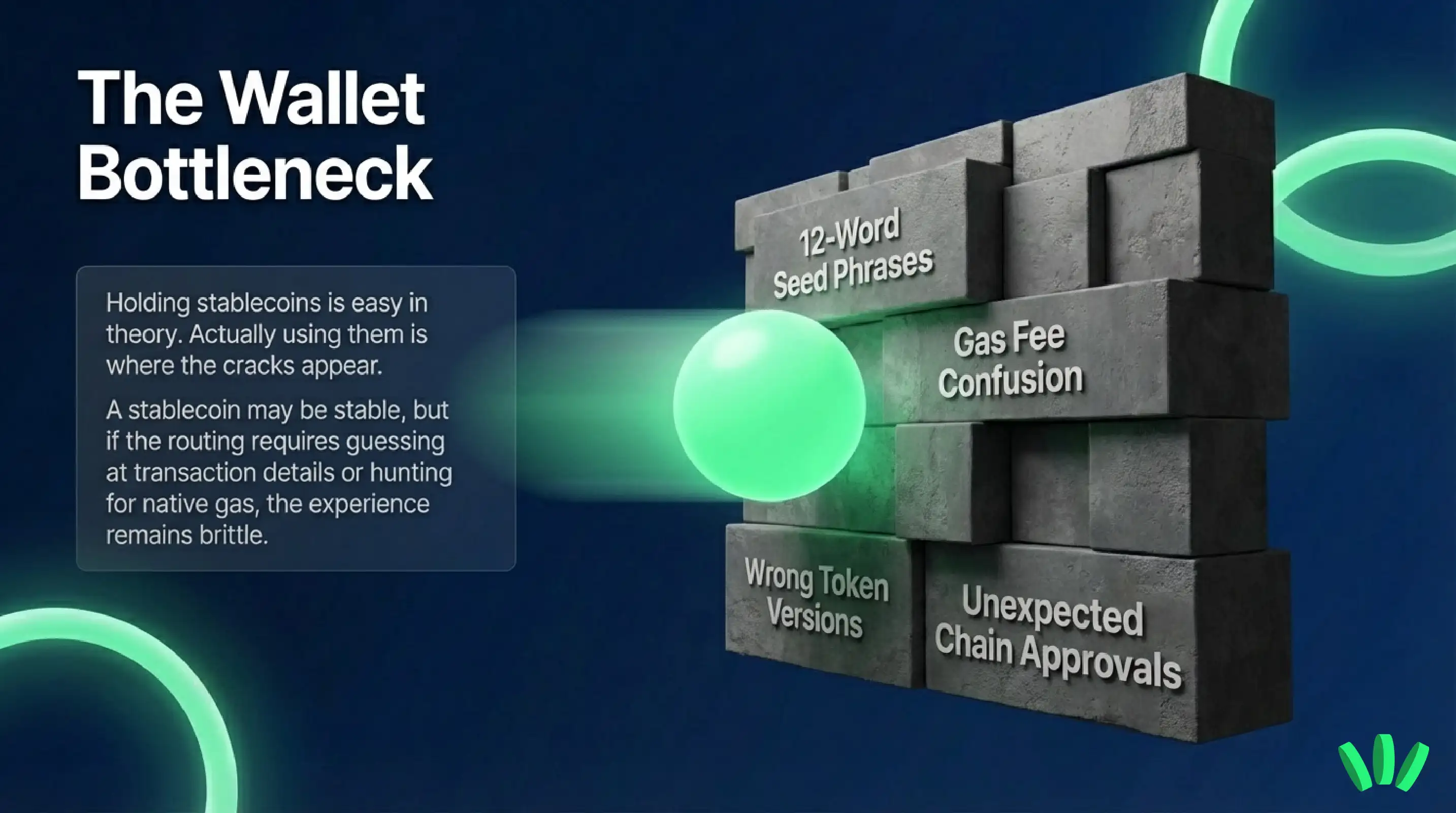

Third, the payment experience can still be messy because blockchain plumbing is messy. A stablecoin may be stable, but that does not mean the route is simple. Wrong network, wrong token version, wrong address type, unexpected gas requirements, approvals you do not fully understand, and bridged asset confusion are still common pain points. This is one reason wallet design matters more than many people assume.

Fourth, regulation is still evolving. The environment is much clearer than it used to be, but it is not finished. The U.S. established a framework for payment stablecoins in July 2025, the UK is working with other regulators on stablecoin rules for payments, and the EU’s framework also warning about spillover risks and cross-border regulatory arbitrage. That is progress, but it is still a moving landscape.

How wallets make or break the stablecoin payment experience

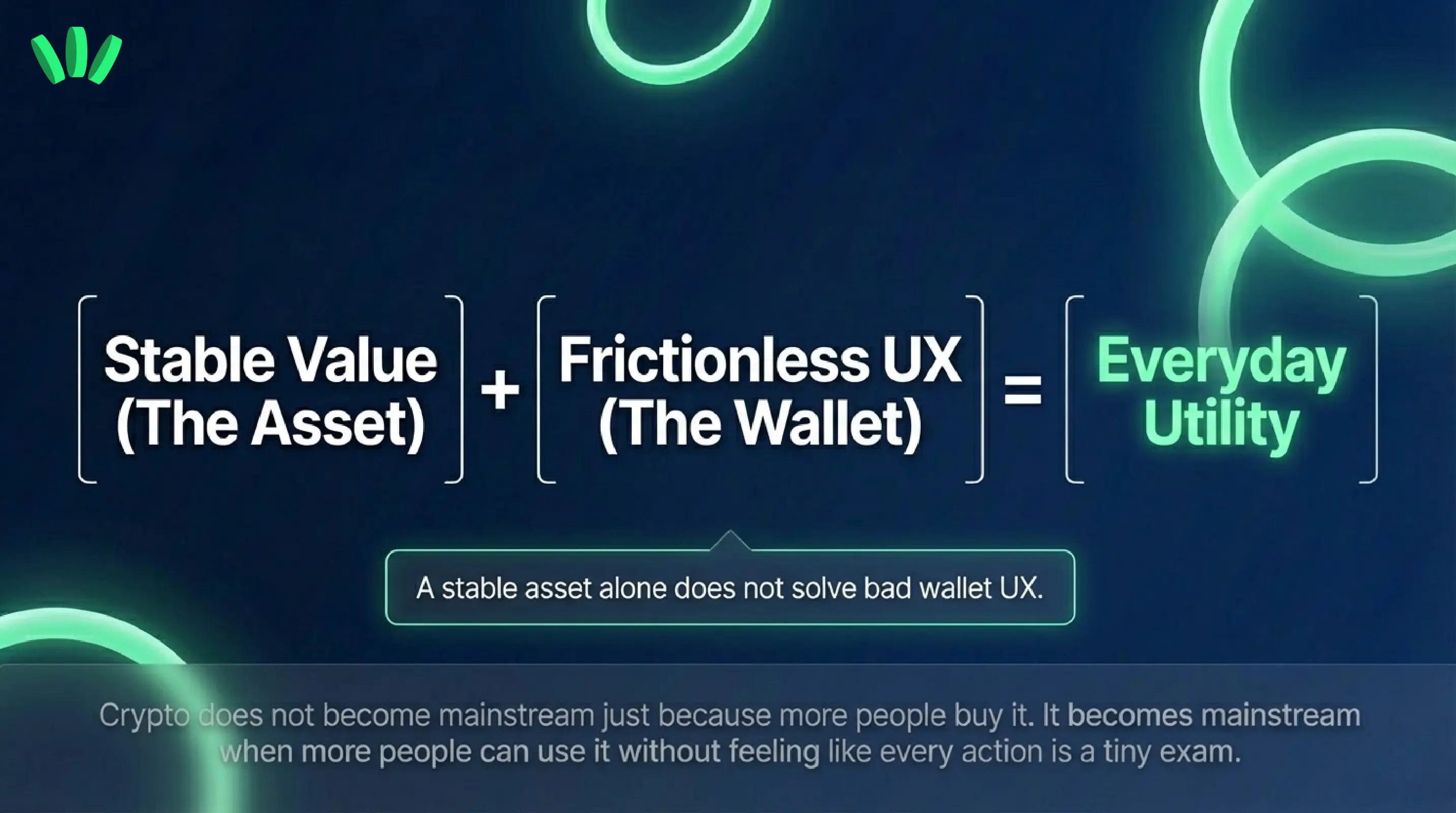

Holding stablecoins is easy to talk about. Actually using them is where the cracks appear. A stable asset alone does not solve bad wallet UX. If a wallet makes you juggle seed phrases, guess at transaction details, hunt for native gas, or second-guess every send, then the asset may be stable while the experience still feels brittle.

Related: Custodial vs Non-Custodial Wallets Explained: Which One Should You Actually Use?

That is where walllet has a strong natural fit inside this topic. walllet.com says it is a non-custodial smart wallet built for crypto and stablecoins across major chains. It also says users can pay transaction fees with any token they own, view activity in human-readable form, create and recover the wallet through passkeys and device ecosystems rather than a traditional seed phrase, and keep credentials on-device with hardware-backed protection. Those are not abstract features. They directly target the friction points that often get in the way of practical stablecoin use.

That changes the experience in a very specific way.

If stablecoins are the asset that makes crypto feel more like money, then wallet UX is the layer that decides whether that promise actually survives contact with reality. A wallet that removes seed phrase friction, reduces gas confusion, and makes transactions easier to interpret gives stablecoins a better chance to feel practical. A wallet that does the opposite turns even the “best” payment asset into another thing you need to babysit.

walllet.com explicitly speaks to “daily users” and says stablecoins can feel more like real money inside a simpler flow.

What is the best crypto for everyday spending?

For most people, the best crypto for everyday spending is a well-supported fiat-backed stablecoin, not BTC and not ETH.

That does not mean Bitcoin or Ethereum are less important. It means they are more effective in different roles. Bitcoin is better framed as a long-term, scarce monetary asset. Ethereum is better framed as the programmable layer that powers onchain applications, tokens, and network activity. Stablecoins are better framed as the spending layer because they reduce volatility, keep value easier to interpret, and fit normal payment expectations more closely.

If you want one sentence to carry forward, use this one: BTC is what many people want to save, ETH is what many people need to use the network, and stablecoins are what many people want to spend.

Why this matters for users who want crypto to feel practical

Crypto does not become mainstream just because more people buy it. It becomes mainstream when more people can use it without feeling like every action is a tiny exam.

Stablecoins matter because they pull crypto closer to ordinary money behavior. They lower one huge source of friction: volatility. But they do not remove every problem. The wallet still matters. The chain still matters. The payment flow still matters. That is why the more interesting question is no longer just “Which coin should I hold?” It is “Which asset-wallet combination makes this actually usable?”

walllet.com fits that shift well. It is building around the idea that self-custody should not feel like punishment. If you want stablecoins to feel more practical, a wallet that reduces seed phrase stress, clarifies activity, and makes gas handling less awkward is not a side detail. It is part of the answer.

Want crypto to feel more practical, not more complicated? Try walllet.com to hold and use stablecoins in a self-custodial wallet built around passkeys, clearer transaction flows, and less day-to-day friction.