Yes, but the real answer depends on the route between your balance and the merchant.

You can hold enough crypto, use a compatible wallet, and still fail at checkout if the asset, network, payment processor, card layer, merchant rules, or settlement path does not line up.

In this article, you will learn how crypto payments work in real life, why a visible balance is not always a spendable route, when stablecoins help, where checkout failures happen, and how wallet UX affects the part of the journey you actually control.

TL;DR

Yes, you can pay with crypto in everyday life, but not always in the way people imagine.

Crypto spending usually follows one of four routes: direct wallet payment, merchant-processor checkout, gift cards or top-ups, and card-linked spending.

Having enough balance does not guarantee checkout success. The asset, network, processor, card layer, merchant rules, and settlement path may still affect whether the payment completes.

Stablecoins reduce price volatility, but they do not remove routing problems. You still need a supported asset, network, checkout path, and merchant route.

Wallet UX matters because it can make the crypto side of the journey easier to understand. But no wallet can force a merchant, processor, or card issuer to approve every payment.

The catch is that “paying with crypto” covers a few very different experiences. In one case, a merchant accepts crypto directly. In another, a payment processor handles the blockchain side and the merchant gets settled in fiat or stablecoins. In card-linked models, the customer may spend from a stablecoin balance while the merchant still gets paid like any normal card transaction. The result can feel simple. The plumbing underneath usually is not.

If you are trying to figure out whether crypto can work like regular money, that is the first mental shift to make. The question is not just “Can I pay with crypto?” It is “Which payment path am I using, who receives what, and how much friction sits between my wallet and the thing I want to buy?”

Method | What it feels like to you | What the merchant usually receives | Best use case | Where the route can fail |

|---|---|---|---|---|

Direct wallet payment | Scan, connect, confirm onchain | Crypto | Crypto-native merchants, digital goods, some online checkouts | Unsupported token or network, gas, confirmations, wrong destination |

Merchant processor checkout | Pay from a wallet through a checkout flow | Often fiat or stablecoins | Ecommerce, invoices, subscriptions | Unsupported wallet, asset or network; processor or settlement failure |

Gift cards or top-ups | Buy value first, then spend normally | Fiat value through an intermediary | Retail brands that do not accept crypto directly | Provider availability, regional limits, extra conversion step |

Card-linked crypto spending | Tap or pay online like a normal card | Fiat through card rails | Everyday retail and travel | Funding step, spending limits, issuer controls, merchant rules, authorization decline |

That is the real landscape today. Crypto spending exists, but the important question is no longer only whether a wallet holds the balance. It is whether the route from that balance to the merchant can actually complete. Some flows are truly onchain. Others depend on processors, conversion layers, card rails, merchant rules, or settlement systems that the user may barely see.

Related: Best Crypto Wallet for Beginners: What to Look for Before You Download Anything

What does “paying with crypto” actually mean?

Most people picture one clean moment: you open a wallet, tap a button, and pay for coffee with Bitcoin or USDC. Sometimes that does happen. More often, there is a translation layer in the middle.

That layer matters because it changes what “crypto payment” really means. For a user, it may still feel like spending crypto. For a merchant, it may look like a normal fiat payment, just with different rails upstream. This is why you will see headlines saying crypto is becoming usable in everyday life, while regular shoppers still feel patchy reality on the ground. Both are true.

The practical takeaway is simple. Crypto payments are no longer fantasy, but they are not one universal experience either. They are a stack of models. Some are great for internet-native commerce. Some are good for cross-border flows. Some work best when you already hold stablecoins. Very few make every in-store purchase feel effortless all by themselves.

How people spend crypto today

People usually spend crypto in four broad ways.

The first is direct wallet payment. This is common in crypto-native environments, certain online merchants, and some invoice or checkout flows. You connect a wallet, confirm a transaction, and the payment happens onchain.

Related: Where Is Your Crypto Actually Stored? Wallet vs Blockchain Explained for Beginner

The second is merchant-processor checkout. Here the merchant does not need to manage crypto deeply. A provider handles the wallet connection, payment routing, and settlement. That is why a business can say “we accept crypto” even if their accounting team still mostly sees fiat or a single stablecoin on the back end.

The third is indirect spending through gift cards, mobile top-ups, or other prepaid value. It is less elegant, but it is often the most accessible bridge between crypto holdings and ordinary spending.

The fourth is card-based spending tied to crypto or stablecoin balances. That is the model most likely to feel familiar to mainstream users because the merchant does not need to care about blockchain at all. Visa’s public work around stablecoin-linked cards shows why this path gets so much attention. It translates crypto into something the retail world already knows how to accept.

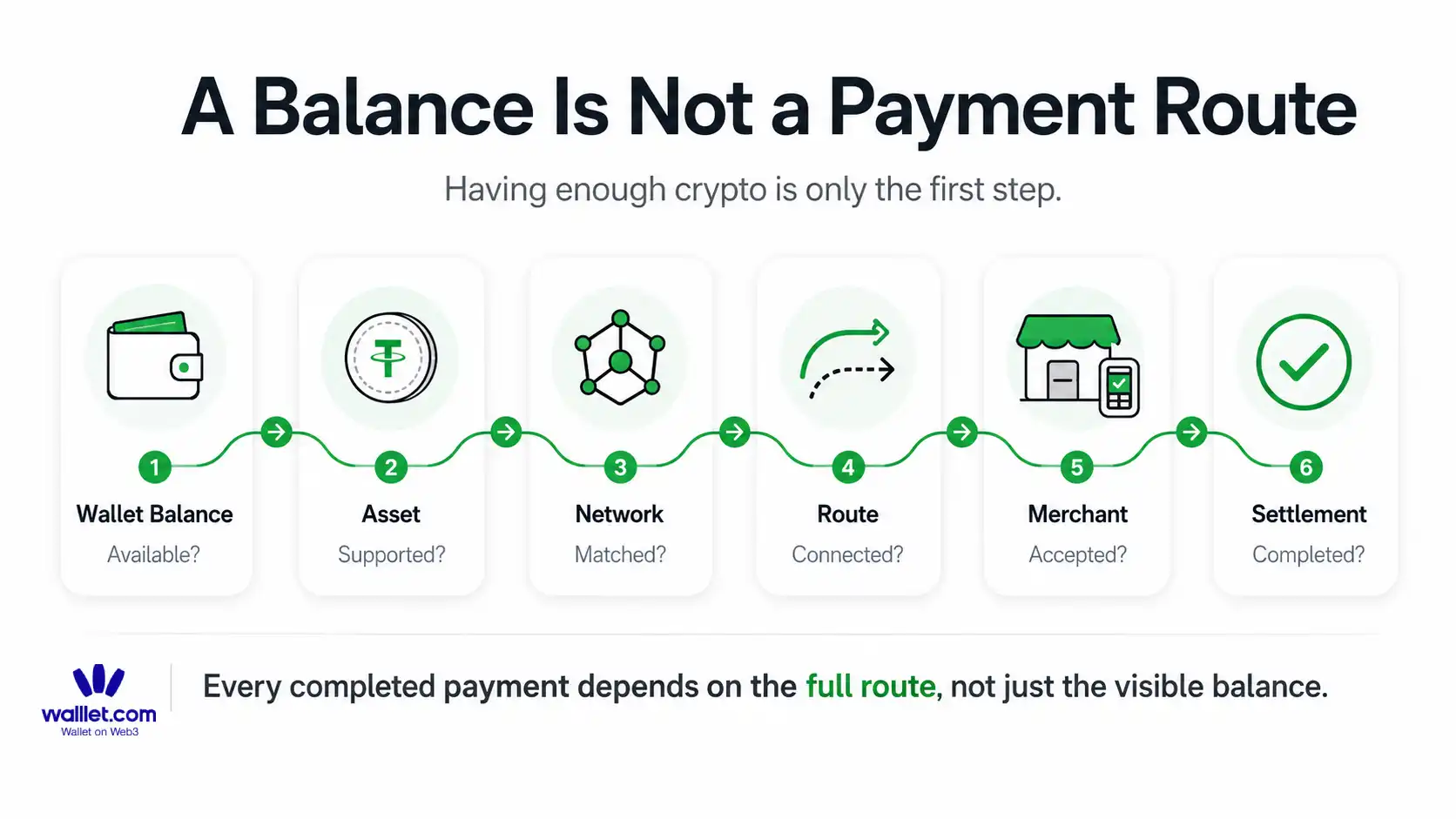

Wallet-to-merchant route: why checkout can fail after balance exists

Having enough crypto in a wallet does not mean a merchant can receive a payment from that balance.

Between “I have the money” and “payment complete,” the transaction may still depend on several layers:

Wallet balance: Do you actually hold the asset you intend to spend?

Asset: Does the checkout support that token?

Network: Is the token on a supported chain?

Route: Is the payment moving directly onchain, through a processor, or through a card-linked flow?

Merchant: Does the merchant accept that payment method, transaction type, country, or currency?

Settlement: Can the payment route complete and settle the merchant in the expected form?

That is the wallet-to-merchant route.

A failure at one layer can stop checkout even when the balance on your screen looks sufficient.

For example:

You hold USDC, but the checkout supports it only on another network.

Your wallet can send the asset, but the payment processor does not support that chain.

You move value into a card-linked spending route, but the final transaction is rejected by an authorization rule.

The merchant accepts the payment method in general, but not that transaction type, region, or card setup.

The route works until one provider has an incident or adds another verification step.

This is why “Do I have enough money?” is often the wrong troubleshooting question.

A better question is:

Which layer of the route failed?

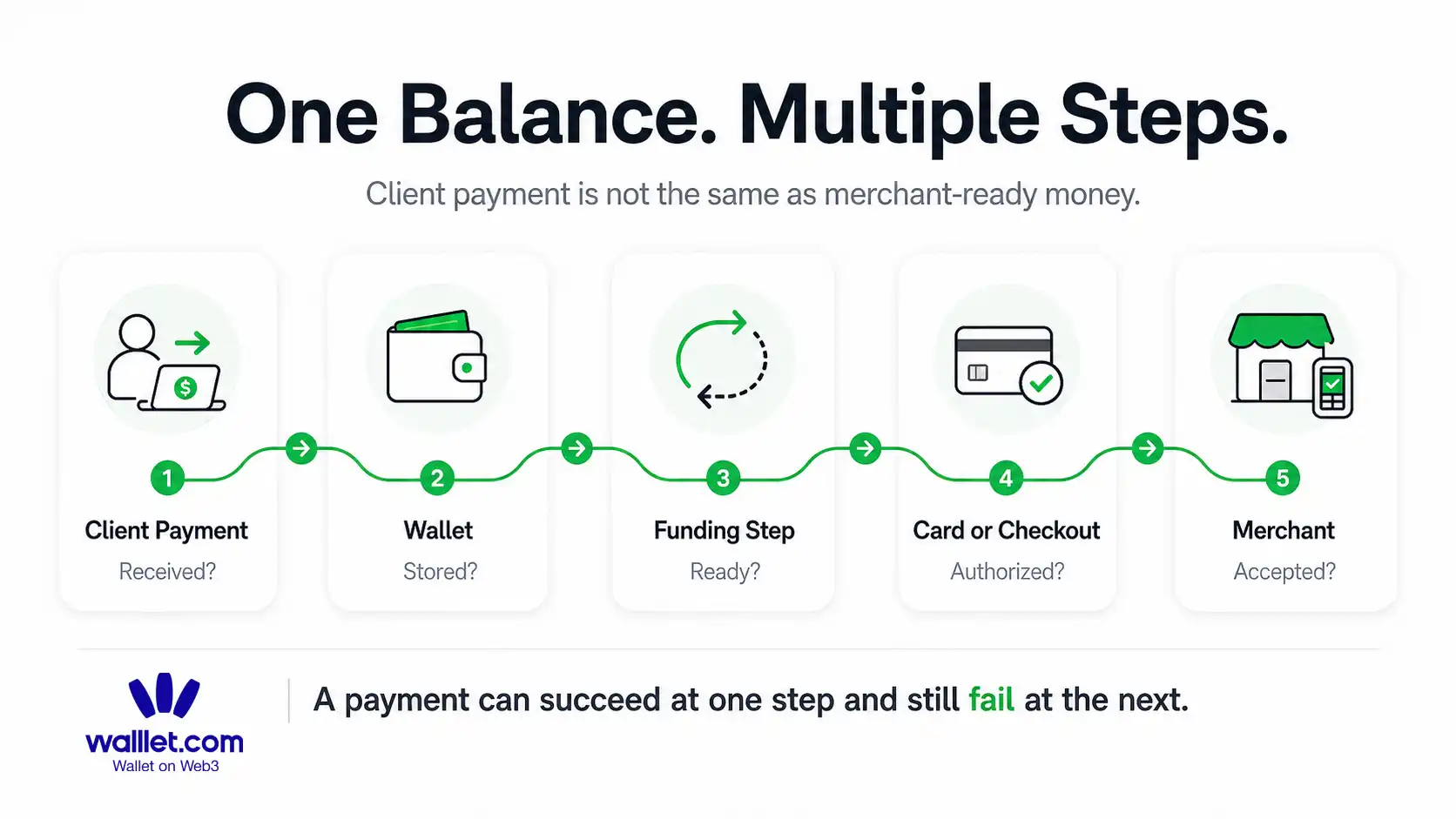

For freelancers and remote workers, the route can be even longer:

Client payment → wallet → swap or funding step → card or checkout → merchant

Each step can work individually while the final payment still fails.

If your money is arriving from international clients in stablecoins, start by mapping the full payment route for freelancer income before deciding how you will spend it.

If the problem happens at the final card or checkout layer, use this guide to understand why crypto cards and virtual dollar cards can be declined even with enough balance.

The practical lesson is simple: do not evaluate only the wallet, only the stablecoin, or only the card. Test the route you actually need to complete.

Can you use crypto like regular money?

Sometimes yes. Completely? Not yet.

Crypto works best as “regular money” when three things are true. You hold an asset you are actually willing to spend. The payment route is accepted where you are shopping. Your wallet makes the process clear enough that you do not feel like you are signing a contract in the dark.

That third point is where many articles go soft. They talk about adoption, merchants, and payment rails, then skip the lived experience. But for an actual user, the wallet is where the whole story either becomes real or collapses into confusion.

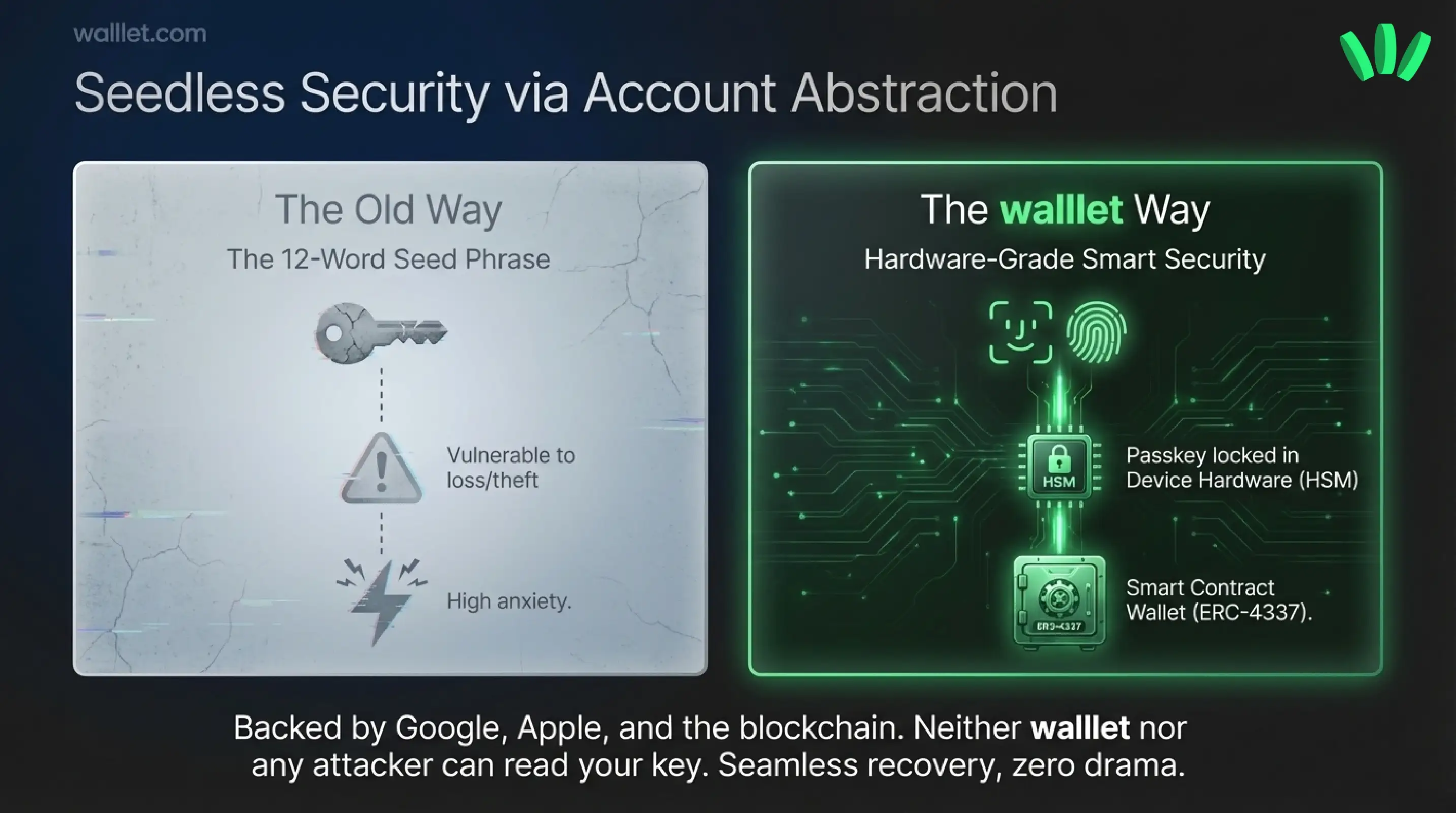

If your wallet makes you worry about seed phrases, unsupported networks, gas tokens, raw contract prompts, or whether one wrong tap will vaporize funds, you are not using crypto like regular money. You are performing a ritual. A bad wallet turns a simple payment into homework.

What makes crypto hard to use for everyday purchases

Once you understand the route, the remaining friction becomes easier to diagnose. Three problems show up repeatedly: price volatility, network mismatch, and wallet or signing friction.

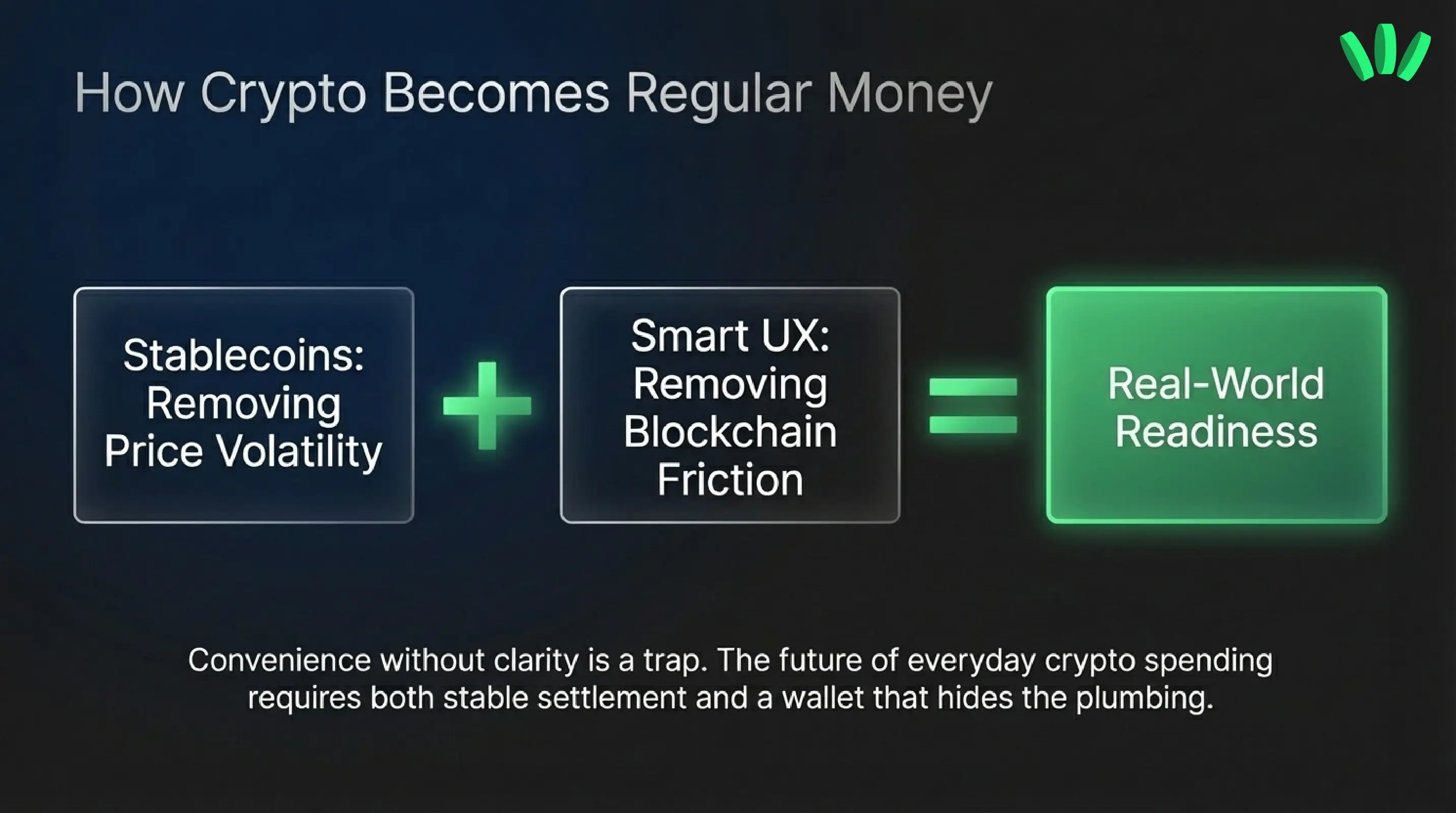

Volatility is the obvious issue. Spending a volatile asset can feel annoying when the price moves sharply before or after the purchase. That is why stablecoins tend to make more sense for daily use. Circle describes USDC as redeemable 1:1 for US dollars and built for always-on digital payments, and merchant guidance from Polygon explicitly notes that stablecoin flows are increasingly central to real-world crypto payments because merchants do not want price exposure during checkout and settlement.

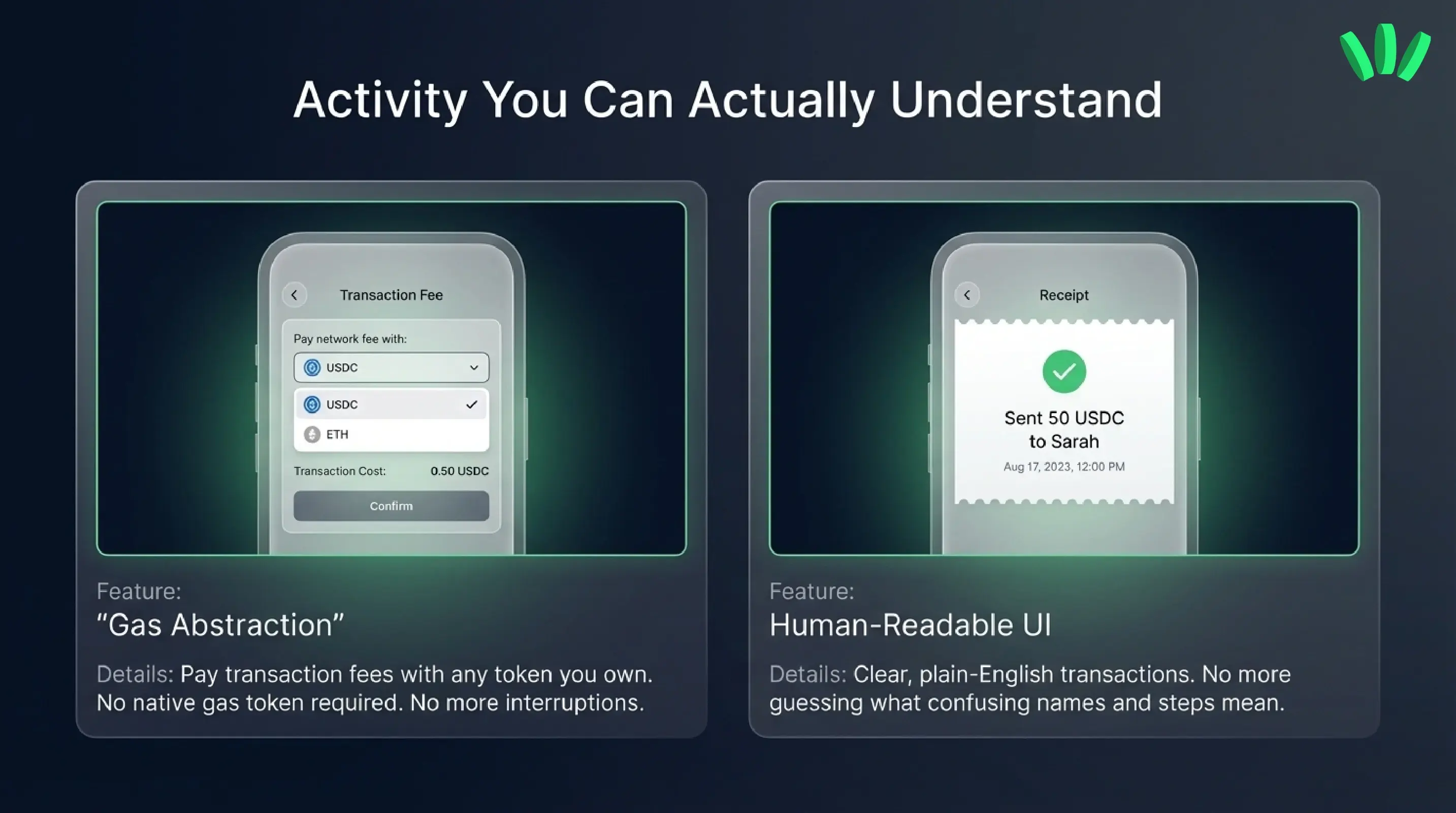

Then there is the network problem. You may have the right value in the wrong place. Maybe the merchant wants one network and your funds sit on another. Maybe you hold USDC but not the native gas token required to move it. Maybe the checkout screen expects a wallet flow you have never used before.

Related: Pay Gas With Any Token: Gas Abstraction Explained

This is exactly where product design stops being cosmetic and starts becoming functional. A wallet that removes seed phrase friction, hides unnecessary complexity, and helps users deal with gas and network confusion is not just more elegant. It is more usable. walllet.com already positions itself around that idea. It is a non-custodial wallet that uses passkeys and biometrics, keeps private keys inside device hardware, supports seedless recovery and sync, and explains gas abstraction in user terms rather than assuming people enjoy memorizing fee mechanics.

There is also a softer problem that becomes obvious fast: refunds, disputes, and mistake recovery. Stablecoin payments can be refunded back to the original wallet, but there is no dispute support in the same way users expect from card chargeback systems. That is great for merchants who want finality. It is less forgiving for consumers used to reversible card-world protections.

Do merchants receive crypto or fiat?

Both models exist, but many businesses prefer not to hold price risk.

That is why merchant processors matter so much. They let the customer pay with crypto while the merchant receives something operationally simpler, often USD, local fiat, or a stablecoin. Visa’s stablecoin-linked card model describes conversion from the user’s stablecoin balance into fiat so the merchant gets paid in local currency like any other transaction.

This matters because it clears up a common misunderstanding. A store can “accept crypto” even when the merchant itself does not want to actively manage crypto treasury. For users, that is fine. You care that payment works. For businesses, it is often the difference between experimenting and saying no.

Direct wallet payments vs merchant processors

Direct wallet payments are closer to the original crypto vision. You pay onchain. The merchant receives crypto. Settlement is native to the blockchain flow.

Merchant processors are more pragmatic. They absorb the complexity and present a cleaner operational result to the seller. For mainstream commerce, that model usually scales better because it asks less from merchants.

If you are a user, the important part is to recognize which mode you are in. Direct payments may offer more native control. Processor-based flows may feel smoother. Neither is inherently better in every case. The best one is the one you can understand and complete with confidence.

Is paying with crypto easier with stablecoins?

Usually, yes.

If your goal is everyday spending, stablecoins remove one mental tax immediately. You do not have to wonder whether you are spending an asset that will jump or drop before dinner. A dollar-denominated balance is easier to reason about. That is one reason stablecoin infrastructure keeps showing up in payment products, merchant tools, and card-linked experiences.

Stablecoins vs volatile assets for spending

Volatile assets still have spending use cases. Some people want to use the asset they already hold. Some merchants prefer broad crypto support. Some users simply do not want to swap first.

But for ordinary purchases, stablecoins are usually the cleaner answer. They make budgeting easier. They reduce “did I just overspend because the market moved?” anxiety. They also fit better with merchant infrastructure built around stable settlement.

That does not mean every stablecoin flow is easy. You still need the right network, a compatible checkout, and a wallet that makes the final approval readable. Still, if someone asks for the best way to pay with crypto from a wallet, stablecoins are often where the practical answer begins.

Why wallet UX matters more than most people think

Imagine two worlds.

In the first, you want to make a simple payment. Your wallet shows a raw prompt, unclear permissions, a confusing network mismatch, and an error because you do not hold the right gas token. You give up.

In the second, your wallet uses familiar login methods, hides seed phrase ceremony, keeps recovery sane, explains what you are approving, and reduces gas friction. Same blockchain. Completely different experience.

That difference is not small. It decides whether crypto feels usable.

This is where walllet.com fits naturally into the topic, even without forcing the product into places it does not belong. walllet.com is built around self-custody without seed phrase sprawl. Its public materials emphasize passkeys, biometrics, hardware-backed private key protection, recovery through Apple or Google account-linked passkey systems, and user-facing clarity around fees and approvals. Its terms and disclaimer pages also make something refreshingly clear: the wallet is non-custodial, blockchain actions are irreversible, and users should pay close attention to approvals, phishing, and what they sign. That combination matters for everyday payments because convenience without clarity is a trap.

A wallet like walllet.com does not magically make every merchant accept crypto. That is not the job. What it can do is make the part you control far less painful. And that is a bigger deal than it sounds.

When paying with crypto makes sense and when it does not

Paying with crypto makes sense when you already keep part of your money onchain, prefer self-custody, want to use stablecoins for real spending, or need a payment path that works across borders and outside bank hours.

It makes less sense when you are using an asset you would rather hold than spend, when the refund path matters a lot, when the checkout flow looks sketchy, or when you do not fully understand what your wallet is asking you to approve.

That last one deserves blunt language. If the payment flow feels unclear, stop. A readable wallet is not a luxury feature. It is a safety feature.

The future of everyday crypto payments will probably look less like “every merchant now lives onchain” and more like a layered system: wallets get better, stablecoins become more common, processors hide complexity, and users stop having to think about the plumbing every time they buy something. That future is already peeking through. It just is not evenly distributed yet.

Before you rely on crypto for a recurring or important payment, test the route you actually need: the asset, network, checkout, merchant, and fallback.

walllet.com belongs in that story because it is not trying to make crypto feel more technical. It is trying to make it feel more usable. For real people, that is the difference that matters. Start with the part you can control: your wallet. Explore walllet.com to see how seedless self-custody, passkeys, and clearer transaction UX can make everyday crypto feel a lot more usable.