The best crypto to spend is rarely the one you’re most excited to hold. If you actually plan to use crypto, not just hold it, the best asset is usually the one that creates the fewest surprises when it leaves your wallet.

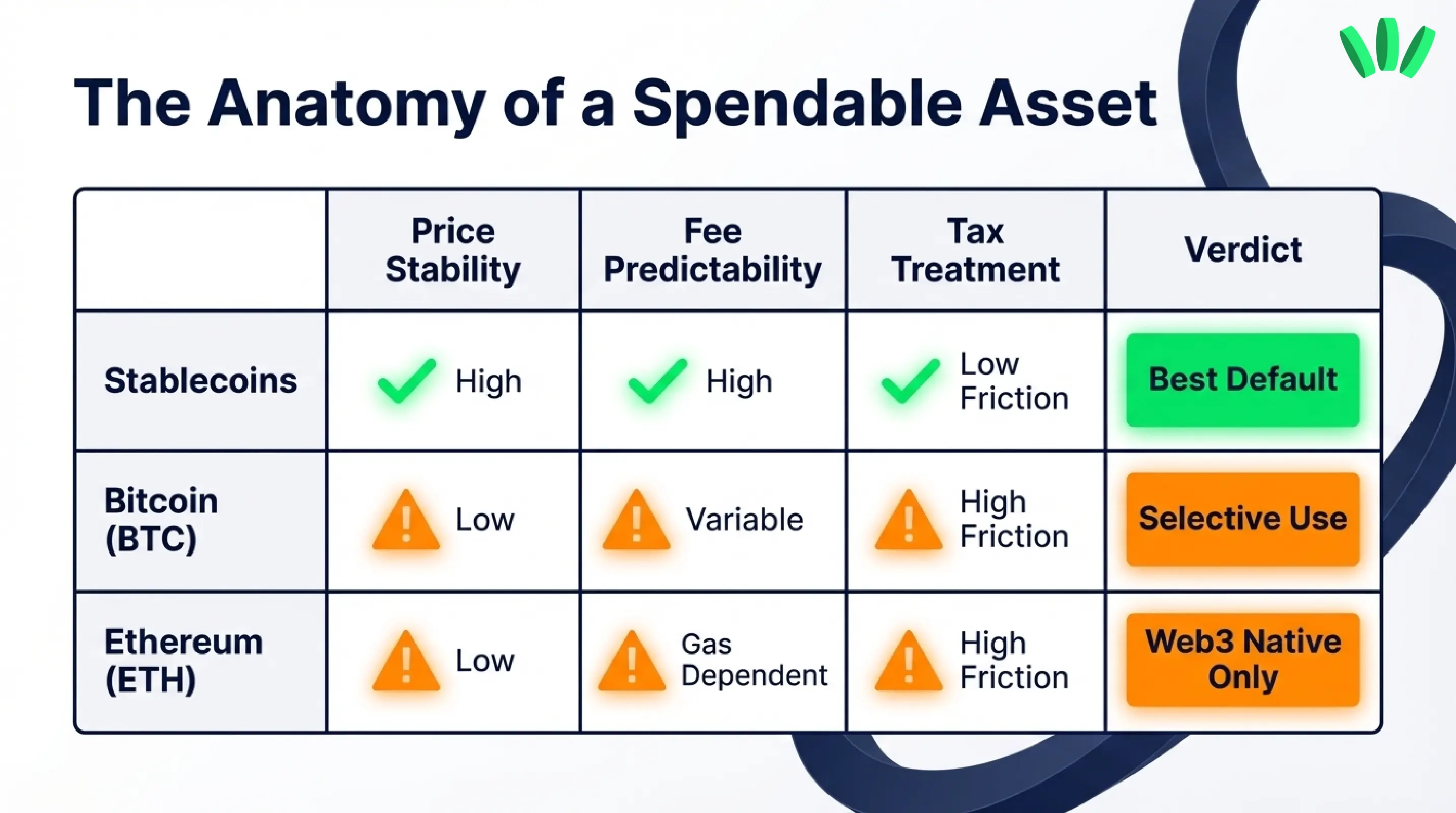

For most people, stablecoins are the best crypto for everyday spending because they keep a steady value and usually make pricing, budgeting, and checkout decisions easier. BTC and ETH can still be spent, but their price swings, fee dynamics, and possible tax consequences often make them less practical for routine payments.

TL;DR

Stablecoins are usually the easiest option for daily spending because they are designed for price stability and are increasingly used in payment flows.

BTC and ETH can work for spending, but they often bring more volatility, more mental friction, and in many jurisdictions, more tax tracking.

ETH adds another layer of complexity because network fees are paid in ETH, and transaction cost can vary with network demand.

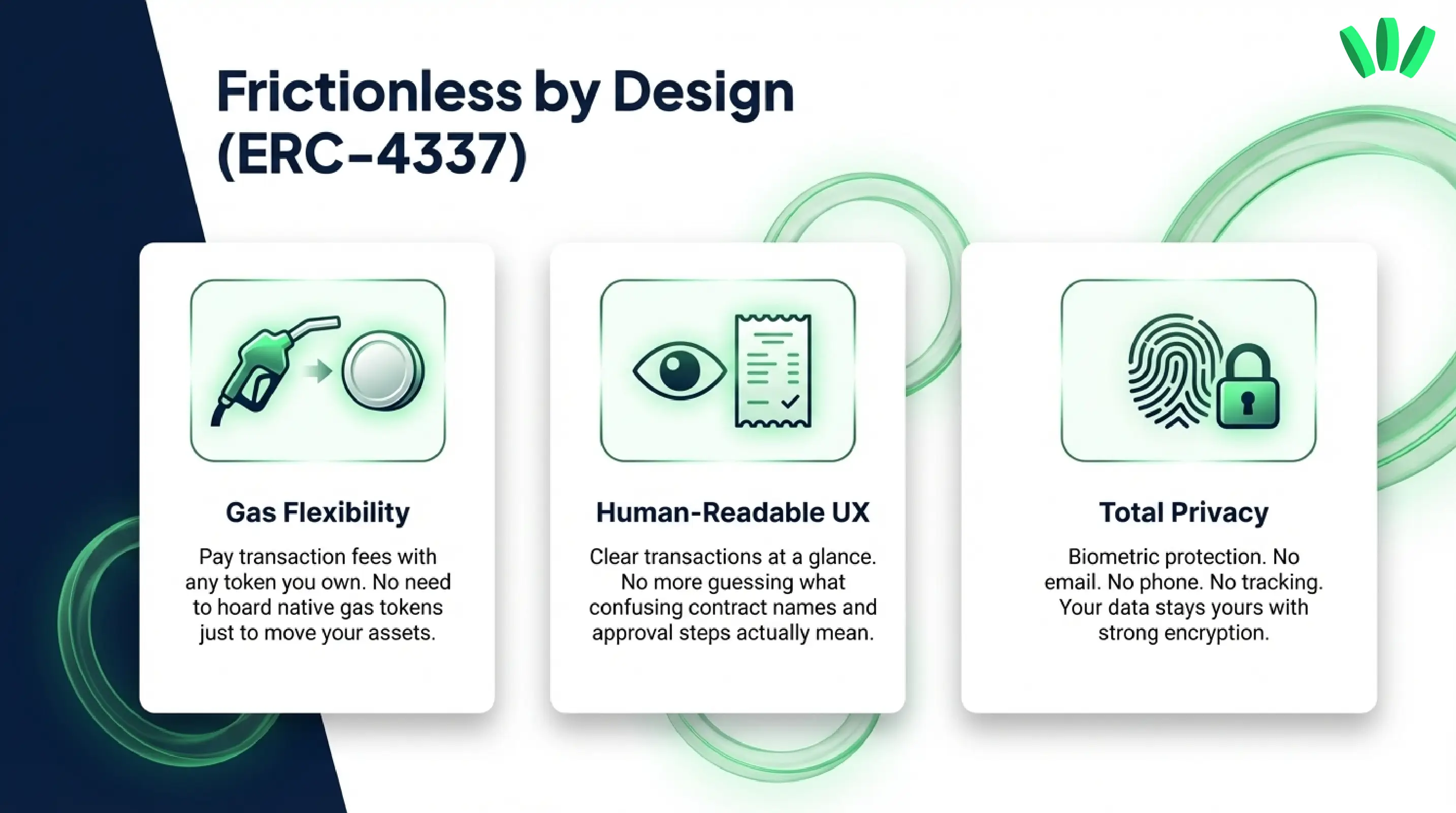

walllet.com is built around making crypto easier to use with passkey-based self-custody, gas flexibility on supported flows, and human-readable transaction prompts that reduce guesswork.

You can spend all three. That is not the hard part.

Related: USDC vs USDT vs DAI or which stablecoin should you use?

The hard part is knowing which asset will still feel like the right choice after the transaction is done. Did the value move? Was the fee annoying? Did you create a tax headache over something as small as lunch? Did you need a separate gas token just to move the asset you already had?

That is why “best crypto for everyday spending” is a different question from “best crypto to hold.” Here’s the short version:

That framework matches how payment-focused industry sources and official documentation separate stablecoins from BTC and ETH: stablecoins are usually positioned as more payment-friendly because they reduce price volatility, while Bitcoin and Ether introduce more uncertainty for day-to-day pricing and accounting.

What makes one crypto better for spending than another?

A spendable asset needs to do something boring really well. It needs to stay understandable while you use it.

Related: Ethereum Wallet: How to Send & Receive ETH and ERC-20 Tokens Safely (Step-by-Step)

That means four things matter more than hype.

First, price stability. If the asset moves sharply between the moment you decide to spend and the moment you check your balance later, it does not feel like everyday money. It feels like a trade you accidentally made.

Second, fee predictability. Bitcoin and Ethereum both involve network fees, but the experience is not identical. Bitcoin fees can vary depending on network conditions and chosen fee rate, while Ethereum fees depend on gas and can rise with network activity. Ethereum’s own documentation explains that transaction cost depends on gas units used and the fee settings attached to the transaction. Bitcoin’s documentation also makes clear that users often choose how much fee to pay when spending.

Third, tax treatment. In some jurisdictions, spending crypto is not just spending. It can count as disposing of property. That means a payment may also become a taxable event. The exact rule depends on where you live, but the broad pattern is real enough that you should never ignore it. The IRS explicitly treats virtual currency as property, and Germany’s finance ministry guidance also treats crypto transactions as potentially taxable depending on the facts and holding period.

Fourth, wallet clarity. Even a good asset can become awkward if your wallet makes networks, fees, approvals, and balances feel murky. This is where product design stops being cosmetic and starts being financial UX.

Why stablecoins are often the easiest place to start

If your goal is everyday spending, stablecoins usually win because they are trying to behave like money, not like a high-conviction bet.

Stablecoins are something people use for online and in-person purchases, transfers, and routine payments. They are useful for faster, cheaper, and more predictable payment flows, even while noting that risks and policy questions still exist.

Price stability vs upside exposure

This is the emotional trap.

People often know stablecoins are better for spending, but still hesitate because BTC or ETH might go up later. Fair. Nobody likes the feeling of spending an asset and then watching it rally.

That is exactly why many users end up with a simple mental split:

hold assets in one bucket

spend-ready assets in another

Once you think that way, the decision becomes cleaner. Stablecoins are not the asset you use because they are the most exciting. You use them because they are the least distracting.

If you want to know whether an asset is good for spending, ask a plain question: do you want this payment to feel like a payment, or like a mini trading decision?

Easy to hold is not the same as easy to spend

BTC is easy to understand as a long-term conviction asset. ETH is easy to justify if you actively use Ethereum or L2 apps. Neither fact automatically makes them ideal for recurring payments.

Spending asks for a different kind of simplicity. You want fewer moving parts, not more. Stablecoins usually give you that by keeping the unit of account closer to the price you see in the real world.

That does not mean every stablecoin is equally good. For spending, the network matters almost as much as the token. A stablecoin on the wrong chain, with thin support in the app or service you use, is not really spend-ready. walllet.com’s own education content already points users toward this kind of practical thinking: what asset is this, on which network, and what will it actually take to move it safely?

When spending BTC or ETH can create more friction

BTC and ETH are not “bad” spending assets. They are just more conditional.

Bitcoin can make sense when you already think in BTC, when the merchant or payment rail is clearly built for Bitcoin, or when you are making a deliberate ideological choice. But for most people, BTC spending comes with a built-in second thought: do I really want to part with this asset now?

Ethereum adds a different kind of friction. ETH is not just an asset. It is also the native token used for gas across Ethereum transactions. Ethereum’s docs explain that fees are tied to gas consumption and fee settings, which means the cost of moving value is not always intuitive to a beginner. And when you are spending an ERC-20 token, you often still need ETH for gas unless your wallet or flow abstracts that away.

Why spending volatile crypto feels harder

Volatile assets create two separate decisions where you wanted one.

Decision one is the purchase itself. Decision two is whether this was the right asset to spend.

That mental split is easy to ignore when markets are flat. It becomes loud when markets move fast. Suddenly a normal transaction carries emotional residue. Maybe you underspent. Maybe you overspent. Maybe you now need to log a gain or loss for something trivial.

This is one reason payment-focused comparisons keep landing in roughly the same place: for actual spending, stablecoins tend to create fewer surprises than Bitcoin.

Asset choice and tax complexity

Tax is where “technically spendable” and “practically spendable” start to separate.

In the U.S., IRS guidance says digital assets are treated as property. Germany’s updated ministry guidance also shows how crypto transactions can carry tax consequences depending on the situation. Local rules differ, but the big lesson is simple: spending crypto can be more than a payment. It may also be a reportable disposal.

That does not automatically make stablecoins tax-free or frictionless. It just means that when price movement is smaller, the accounting pain often feels more manageable than it does with BTC or ETH.

Fees, volatility, and taxes before you choose an asset

Before you decide what sits in your spend-ready balance, run a quick filter.

If you need price certainty, use a stablecoin.

If you need deep conviction exposure, keep BTC or ETH in your hold bucket.

If you need to interact with Ethereum apps, keep some ETH because network usage still revolves around native gas, even if newer wallet designs can soften that experience on supported flows.

And if you care about staying sane, separate the asset you want to grow from the asset you want to spend.

That sounds obvious. In practice, it saves people from a lot of self-inflicted friction.

How walllet.com can help users manage spend-ready assets more clearly

A good wallet should not just store assets. It should help you understand what you can actually do with them.

That is where walllet.com fits naturally into this topic.

walllet.com positions itself as a non-custodial smart Web3 wallet built to send, receive, and store crypto and stablecoins across major chains. Its product pages and educational articles emphasize passkey-based setup, biometric access, no seed phrase, hardware-backed key protection on the device, gas flexibility on supported flows, and human-readable transaction prompts. The core idea is simple: reduce friction without taking control away from the user.

That matters when you are managing assets for different jobs.

A wallet that helps you see what you hold, what network it is on, what fee model applies, and what you are about to sign makes it easier to keep a clean split between long-term assets and spend-ready assets. It also makes stablecoins feel more usable for the people who actually want crypto to function like real money, not just portfolio wallpaper.

If your goal is everyday crypto use, that clarity matters more than another giant list of supported tickers.

The better question is not “Can I spend BTC, ETH, or stablecoins?”

You can.

The better question is “Which one lets this payment stay a payment?”

For most people, that answer still points to stablecoins first, BTC second when the context fits, and ETH mostly when the transaction is tied to Ethereum-native activity rather than ordinary day-to-day spending. A wallet like walllet.com helps because it is built around making those choices easier to understand before you tap approve.

Keep your long-term holds and your spend-ready assets clear. Create your walllet with passkey-based self-custody, manage stablecoins and crypto across chains, and review transactions with less guesswork before you approve.