Stablecoins are most useful when they solve a specific money problem.

You can receive income in USDT or USDC, hold part of it in dollar-pegged value, send money across borders, pay through supported cards or apps, and convert what you need for local spending.

The mistake is treating one Stablecoin balance as savings account, payment account, trading capital and emergency fund at the same time.

For freelancers, the most practical starting point is the guide to receiving USDT or USDC from international clients. If you are still choosing between the main assets, compare USDT, USDC and DAI before moving serious money.

What stablecoins are useful for

USDT and USDC are Crypto assets designed to track the US dollar. They can move through supported Blockchain networks without using a conventional bank transfer for every transaction.

They do not work like insured bank deposits. Their value and usability depend on the issuer, reserves, Token contract, Blockchain network, liquidity, Wallet and services used to convert or spend them. The useful question is not whether Stablecoins are “good” or “bad.” It is whether they fit the job you need done.

Use | Best fit | Check before using |

Receiving income | Clients already comfortable with USDT or USDC | Token, Network, Wallet and later cash-out route |

Holding dollar value | Short-term income or spending reserves | Issuer, custody, recovery and depeg risk |

Spending online | Supported cards, apps or merchants | Fees, limits, region and settlement currency |

Sending money | Transfers between supported Wallets or services | Recipient, Network and total cost |

Cashing out | Converting part of a balance for local use | Rate, spread, fee, timing and account requirements |

Swapping | Moving into the Token required for the next step | Final received amount, gas, Slippage and approvals |

Stablecoins work best as a route, not as an isolated balance:

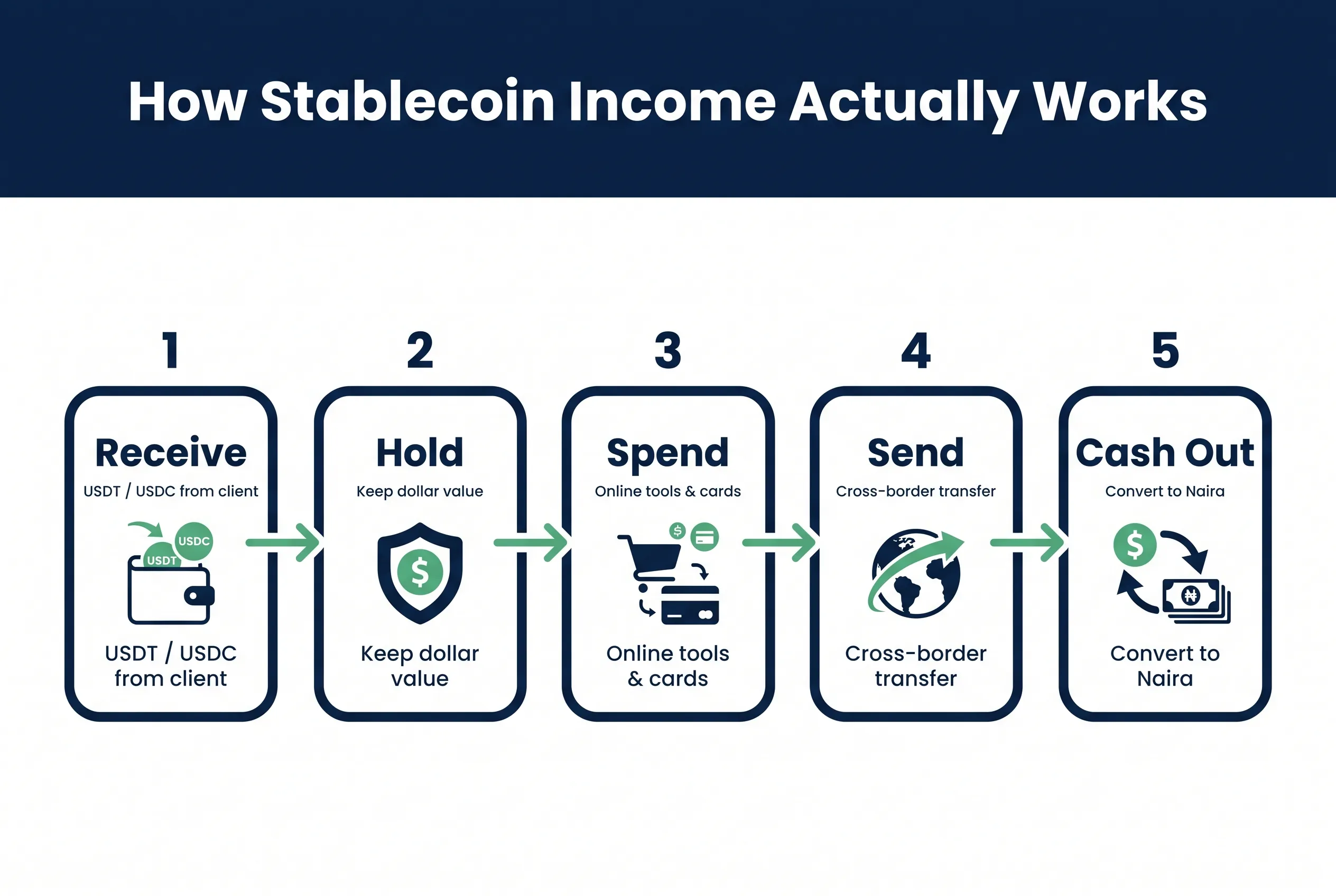

Receive → Hold → Spend, send or cash out

1. Receive freelance or remote-work income

Stablecoins can be practical when a client already holds USDT or USDC or regularly pays contractors through Crypto.

They become less practical when the client must open an exchange account, buy a Token, choose a Blockchain network and learn Wallet security merely to pay one invoice.

Before accepting a Stablecoin payment, agree on:

USDT or USDC

Exact Blockchain network

Invoice amount

Receiving address

Fee responsibility

Test-transfer requirement

Transaction Hash after payment

A Wallet address alone is incomplete. The client needs the Token and Network as well.

Use the Stablecoin payment checklist for freelancers before sharing payment instructions. If the chain is unclear, compare the available networks for sending USDT or USDC. Stablecoin payments are most useful when you have already planned the next step. Receiving $1,000 in USDT is not useful if your Wallet supports the transfer but your spending or Cash-out route does not support the same Network.

2. Hold part of your income in dollar value

A Nigerian freelancer may not want to convert every foreign payment to Naira immediately. Holding part of an income balance in USDT or USDC can keep money available for:

Software subscriptions

Hosting and cloud services

Advertising

International contractors

Travel expenses

Future invoices priced in dollars

Later conversion to local currency

This is different from investing. A Stablecoin usually aims to preserve dollar-denominated value. It does not automatically generate a return. If a platform offers interest or Yield, the user is taking additional custody, lending, liquidity or Smart Contract risk.

Keep the amount tied to a clear purpose. Monthly work expenses, near-term reserves and experimental DeFi funds should not sit in the same place. The guide to holding digital dollars during local-currency inflation examines this use case in more detail.

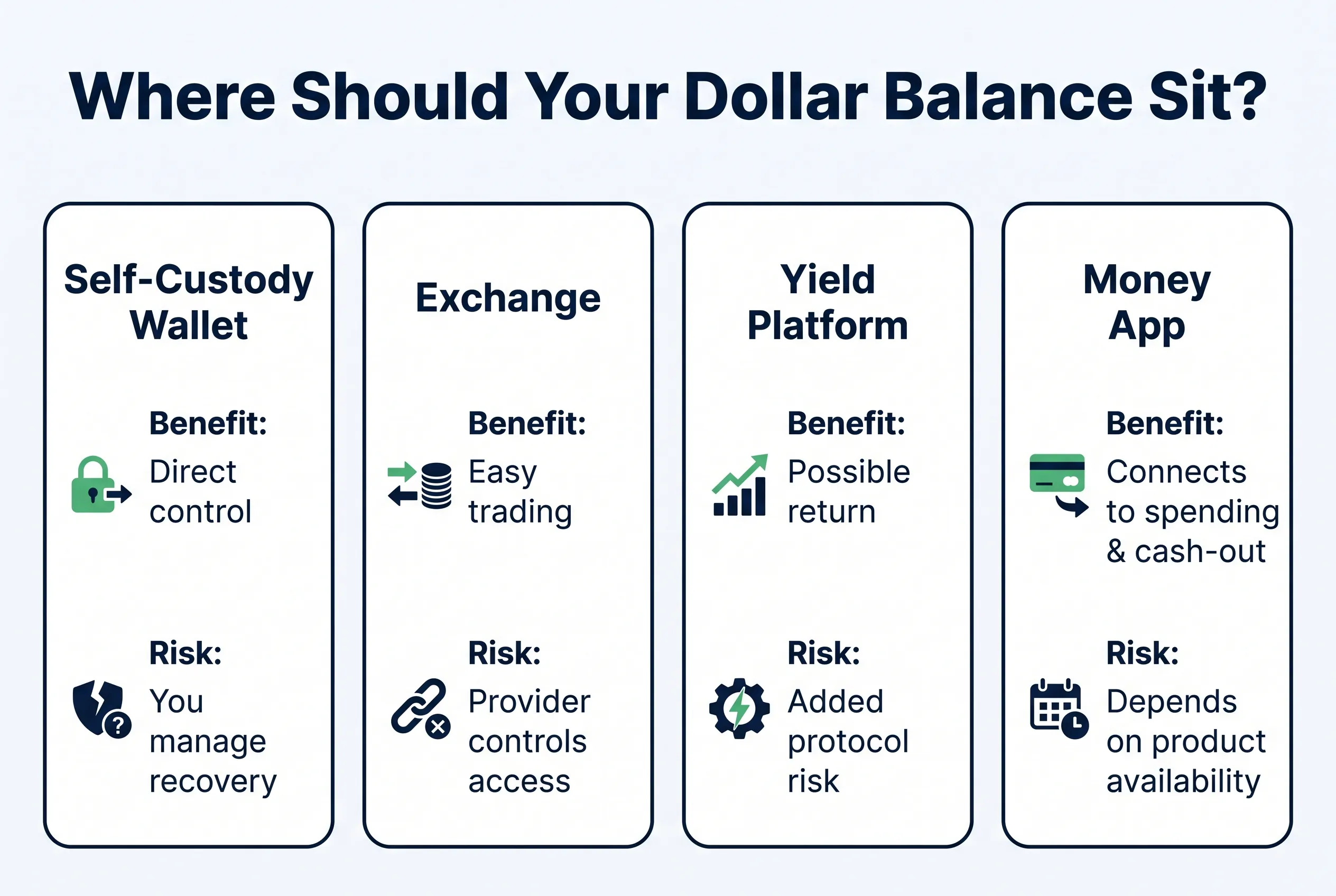

Choose where the balance sits

Location | Main benefit | Main risk |

Self-custody Wallet | Direct control over transactions | User manages recovery, security and networks |

Exchange | Easy trading and conversion | Provider controls access and withdrawals |

Yield platform | Possible return | Added custody, liquidity and protocol risk |

Money app with Stablecoin infrastructure | Can connect holding with receiving, spending or Cash-out | Availability and control depend on the product layer |

Self-custody does not remove every Stablecoin risk. Issuers may retain controls over particular Tokens and addresses. The differences are explained in whether USDT or USDC can be frozen.

3. Pay for online tools and services

Stablecoins are rarely accepted directly by every website a freelancer uses. Spending usually happens through one of three routes:

A merchant accepts the Stablecoin directly.

A payment app converts or settles the payment.

A supported virtual or physical card uses the balance behind the scenes.

Before relying on a Stablecoin spending route, check:

Card or merchant availability → Supported countries → Transaction currency → Conversion rate → Card funding fee → Spending limits → Merchant-category → restrictions → Refund process → What happens when a transaction is declined

A successful Stablecoin deposit does not guarantee that every card transaction will work. The card issuer, merchant, settlement currency, available balance and compliance checks still affect the payment. Do not move the entire balance into a spending account. Keep only the amount needed for near-term purchases.

4. Send money across borders

Stablecoins can move dollar-pegged value between supported Wallets without waiting for conventional international banking hours. That does not make every Stablecoin transfer cheap or simple. The full cost may include:

Purchase or funding cost + Blockchain fee + receiving fee + conversion spread + local Cash-out fee

Before sending, confirm:

Exact recipient address

Stablecoin

Blockchain network

Amount

Native Token needed for Gas

Whether the recipient can use that Network

Whether a Memo or Destination Tag is required

Whether a small test transfer is sensible

The sender and recipient should choose the route together. Selecting the cheapest Blockchain fee is pointless when the recipient cannot use or Cash out the asset. For smaller transfers, compare the complete cost rather than the Network fee alone. The guide to the cheapest and safest way to send USDT or USDC covers that calculation.

5. Convert only what you need

Stablecoins are useful when they let the user choose when and how much income to convert. Instead of converting an entire payment immediately, a freelancer may:

Keep part for dollar expenses

Use part for online subscriptions

Transfer part to another Wallet

Convert part to Naira for local costs

The relevant figure is the final amount received after all costs. Compare: Exchange rate, spread, fixed fee, percentage fee, network cost, minimum amount, processing time, account review risk, and bank or Cash-out destination

A quoted rate can look attractive while the final payout is worse after fees. Check the exact amount that will arrive before confirming.

6. Swap USDT and USDC only when it solves a problem

USDT and USDC both aim to track the dollar, but they are not interchangeable across every Wallet, Network, card or payment service. A Swap may make sense when:

A spending route accepts USDC but not USDT

A client paid through a Token your next service does not support

Your destination requires a different Stablecoin

You prefer the issuer and reserve model of the other asset

A same-network Swap avoids a more complicated withdrawal route

Do not Swap because one Token currently sounds more fashionable.

Check:

Whether the Swap stays on the same Network

Gas fee

Swap fee

Slippage

Final amount

Token approval

Whether a Bridge is involved

Whether the destination already accepts the current Token

The USDT-to-USDC Swap guide explains when the conversion is worth its cost.

How walllet.com Connects Dollar Income to Spending and Cash-Out

Stablecoins are most useful to freelancers when they fit inside the complete income cycle. Receiving a Token is only the first step.

walllet.com is designed as a USD money app for Nigerian freelancers and remote workers. Its intended workflow connects:

Receive global income → hold value in dollars → spend online → cash out to Naira

Stablecoin and self-custody infrastructure support parts of that experience, but the product is not positioned as a general Crypto Wallet or Trading app. For eligible users, walllet.com can bring several stages into one product:

Receive supported international payments

Keep part of the balance in dollar value

Use supported spending routes

Convert the amount needed for local use

Manage supported onchain assets without a traditional Seed Phrase workflow

The exact receiving currencies, payment rails, Stablecoins, networks, cards, rates, limits and Cash-out routes depend on what the current account shows.

This matters because the real alternative is often a stack of separate services: one app to receive, another Wallet to hold, a card app to spend and another provider to convert to Naira.

See how walllet.com can connect Stablecoin holdings with the way you use global income.

Stablecoin risks to keep separate

Stablecoin risk is not one single problem.

Risk | What can happen |

Issuer risk | The issuer can face reserve, operational or legal problems |

Depeg risk | The Token can trade below or above its intended value |

Network risk | A transfer can use the wrong chain or face congestion |

Wallet risk | Access can be lost or a malicious transaction approved |

Custody risk | An exchange or platform can restrict access |

Liquidity risk | The asset may be difficult or expensive to convert through a particular route |

Regulatory risk | Local rules or provider requirements can affect availability |

Smart Contract risk | A contract or protocol can fail or be exploited |

Circle states that USDC is backed by highly liquid cash and cash-equivalent reserves and publishes reserve information and third-party assurance reports. Tether states that USDT is backed by its reserves and publishes reserve reports. These are separate issuers with different structures, disclosures and legal terms.

Check the issuer’s current documentation rather than assuming every dollar-denominated Token carries the same risk.

Be careful with Stablecoin Yield

Yield does not come from the Stablecoin merely existing. It may come from:

Lending

Exchange programs

Liquidity pools

Token incentives

Treasury-backed products

DeFi Vaults

Each route adds another party, contract or liquidity condition.

A high APY is compensation for some form of risk, even when the interface presents it as ordinary savings. Do not move income needed for rent, taxes, payroll or near-term expenses into a product you cannot explain.

Use separate balances for separate jobs

A practical Stablecoin setup does not require one Wallet to do everything. You may keep:

A receiving balance for client payments

A short-term dollar reserve

A spending balance

A small amount for Network fees

A separate Wallet for DeFi or experimental activity

A separate route for local Cash-out

This improves recordkeeping and limits exposure to unsafe approvals. The receiving Wallet should stay predictable. Client payments do not need to share an address with every Token experiment the internet invents before breakfast. Use walllet.com to connect supported global payments, dollar-value holding, online spending and local Cash-out in one income workflow.