If yield is the promise, hidden risk is the price tag.

For most cautious users, staking is usually easier to reason about than lending, but it is not automatically safer in every case. Staking pays you for helping secure a proof-of-stake network. Lending pays you for taking borrower and platform risk. The better choice depends on what you hold, how soon you may need liquidity, and how much hidden risk you can tolerate.

Staking vs lending is not just about APY. Compare risk, liquidity, lockups, slashing, lending exposure, and what to check in your wallet before you commit.

TL;DR

Staking and lending both generate yield, but they work for completely different reasons. Staking earns protocol rewards. Lending earns interest from borrowers.

For beginners, staking is often the simpler mental model, especially when you already planned to hold a proof-of-stake asset long term.

Lending can offer flexibility or fit assets like BTC and stablecoins, but it adds counterparty, platform, and smart contract risk depending on the route you use.

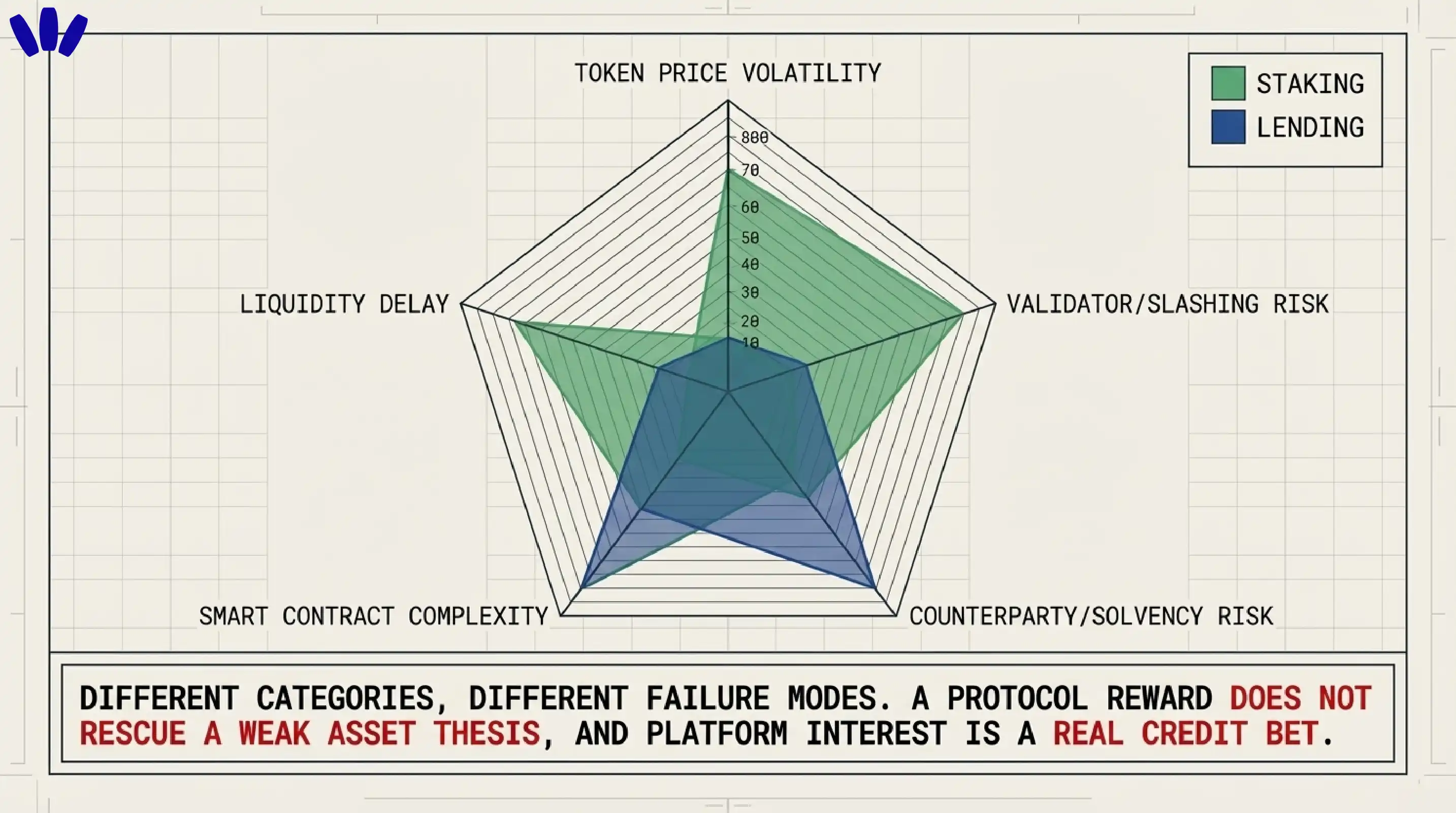

You can lose money in both. With staking, losses can come from price drops, lockups, validator issues, slashing, or smart contract risk in liquid staking. With lending, losses can come from borrower defaults, insolvency, liquidation cascades, or protocol exploits.

The wallet layer matters more than most comparison articles admit. Before you deposit anywhere, you want clear approvals, readable transaction details, chain clarity, and fewer chances to sign blind. That is where walllet.com fits naturally.

If you searched “staking vs lending,” you want to know which one is safer, which one is more liquid, and where people usually get burned. That is the right frame. Here is the short version before we go deeper.

Question | Staking | Lending |

What are you getting paid for? | Helping secure a proof-of-stake network | Letting a borrower or platform use your assets |

Main risk | Token price risk, validator risk, lockups, slashing, liquid staking smart contract risk | Counterparty risk, platform solvency, smart contract risk, liquidation and liquidity mismatch |

Liquidity | Often delayed by unbonding or withdrawal queues | Sometimes more flexible, but depends on platform structure |

Best fit | Long-term holders of PoS assets who understand the network they hold | Users seeking yield on non-stakeable assets like BTC or on stablecoins, and who understand platform risk |

Typical beginner mistake | Chasing APY without understanding lockups or liquid staking complexity | Treating lending yield like a savings account and ignoring who actually holds the risk |

That framing explain staking and lending, but rarely explain how a user should evaluate the approval screen, the route, the contract exposure, or the crypto wallet experience before committing funds. For a product like walllet.com, that gap matters.

Related: Best Crypto Wallet for Beginners: What to Look for Before You Download Anything

What is Staking & How it works

Staking means locking or delegating a proof-of-stake asset so it helps secure the network and, in return, earns rewards. In the simplest version, you are not lending your coins to a borrower. You are participating in the economics of the chain itself. That is why staking only applies to proof-of-stake assets, not everything in your portfolio. Bitcoin, for example, is not a staking asset.

That cleaner mental model is one reason cautious users often gravitate toward staking first. If you already planned to hold ETH, SOL, ADA, DOT, or another PoS asset for months anyway, staking can feel like an extension of holding rather than a separate credit bet. Still, “cleaner” does not mean “risk free.”

Validator and slashing risk

When you stake, rewards depend on network rules and validator performance. Some networks can slash validators for serious misconduct, and that can reduce the stake tied to them. Slashing is a forced removal with loss of staked ETH, and some or all of your staked assets can be lost in certain scenarios depending on the cause and setup.

Related: What is Ethereum and how does it work?

For most retail users, slashing is not the only risk that matters. Price risk is often bigger. A 5% to 8% annual reward looks nice until the token itself falls 30%. Staking pays in the same asset you are already exposed to. That is great when conviction and timing are aligned. It is less comforting when they are not.

What is Lending & How it works

Lending is different at the root. You are not helping a network reach consensus. You are making assets available to borrowers, either through a centralized platform or a DeFi protocol, in exchange for interest. That means your return depends on borrower behavior, platform design, collateral rules, and the structure sitting between you and your assets.

This is why lending often makes more sense for assets that cannot be staked, especially BTC, or for stablecoins when a user wants yield without direct exposure to a volatile PoS token’s reward structure. But the comforting word “interest” can be misleading. Crypto lending is not a plain savings product in different clothes. It carries real credit, liquidity, and platform risk.

Counterparty and smart contract risk

In CeFi lending, the biggest question is who is borrowing, how the platform manages risk, and what happens if too many users want out at once. In DeFi lending, the focus shifts toward overcollateralization, smart contracts, liquidation mechanics, oracle dependencies, and systemwide contagion during volatile periods. Liquidation risk, operational risk, and complexity as meaningful concerns in crypto lending markets.

DeFi lending typically relies on overcollateralized structures because crypto collateral can drop quickly in value.

That distinction matters because “lending” is not one thing. A centralized platform lending your assets to institutional borrowers and a DeFi pool using automated collateral rules are not the same risk package. Same headline category, very different failure modes.

Staking vs lending: risk, liquidity, and return comparison

If you strip away the marketing, this decision comes down to three levers: what kind of risk you are taking, how fast you may need your money back, and whether the reward justifies the complexity.

For most beginners, staking is usually the easier model to audit mentally. You hold a PoS asset, you understand the network, you accept lockups, and you earn protocol rewards. Lending can be perfectly reasonable, but it requires you to trust a borrower set, a platform, or a contract system.

Staking often feels more “asset-native,” while lending feels more “financial-product-native.”

That does not make staking automatically safer. A volatile token with a long unstaking delay can be a worse fit than conservative stablecoin lending for some users. Context decides the answer.

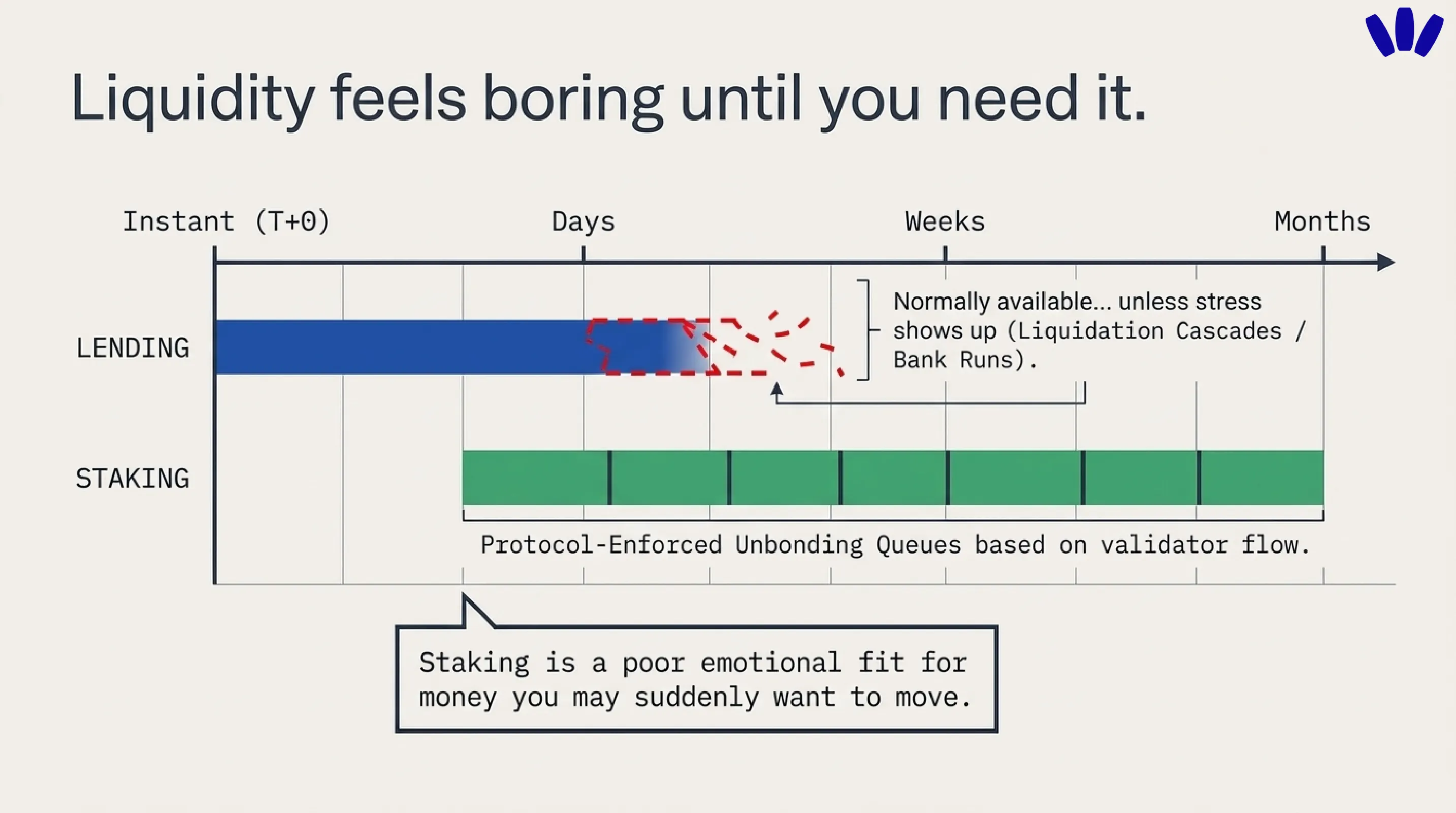

Lockups and withdrawal times

Liquidity is where many comparisons get too casual. Staking frequently involves unbonding or withdrawal delays. Ethereum’s withdrawal process depends on validator flow and queue conditions, and even large-scale withdrawal throughput is constrained by protocol mechanics. Also unstaking can take from hours to weeks depending on the asset and network conditions.

That means staking is a poor emotional fit for money you may suddenly want to move. If you are the kind of person who watches the market, panics, and wants optionality, staking can feel calm right up until the moment you want out.

Lending may look more liquid on paper, but you still need to ask whether withdrawals are truly available on demand or merely “normally available unless stress shows up.” That difference has mattered more than once in crypto history, and cautious users should treat it as a first-order question, not a footnote.

Native staking vs liquid staking vs lending

This is where the comparison gets sharper.

Native staking is the cleanest version. You stake the asset directly or delegate it to a validator. The trade-off is straightforward: rewards plus lockup and validator risk.

Liquid staking adds a wrapper. You stake the asset, receive a token that represents that staked position, and may keep using that token elsewhere. That improves flexibility, but it also adds smart contract, peg, and protocol-composability risk. The EBA-ESMA factsheet specifically flags additional market volatility and disclosure concerns around liquid staking tokens.

Lending is a different lane. You are not extending a staking position. You are exposing assets to a borrower or pool structure in exchange for interest.

If you are cautious, the ranking usually goes like this: native staking is easier to reason about than liquid staking, and liquid staking is usually easier to reason about than strategy-stacked lending or restaking combinations. More moving parts can create more yield, but they can also create more ways to misunderstand what you just signed.

Is staking safer than lending?

Usually, yes, for a cautious beginner who already holds a PoS asset and understands the chain. But the honest answer is “safer in what sense?”

Staking often has fewer layers of counterparty exposure than lending. You are mainly dealing with token risk, validator quality, and protocol mechanics. Lending adds borrower quality, platform solvency, collateral health, smart contracts, withdrawal structures, and sometimes opaque risk management. That is why many comparison pages and market explainers present:

staking as the simpler path for long-term PoS holders, while lending suits different assets and different goals.

Still, safer does not mean profitable. If you stake a volatile token you never truly wanted to hold, the staking reward can become lipstick on a bad position. That is one of the most common mental traps in this category.

Can you lose money staking?

Yes.

You can lose money staking because the asset price drops, because your funds are illiquid during an unstaking window, because a validator is penalized, or because a liquid staking route introduces smart contract or depegging risk. Slashing and penalties directly, and multiple mainstream staking explainers now answer this question plainly rather than pretending rewards cancel risk.

Staking is not a shield against a bad asset thesis. It is a yield layer on top of an asset you already own. If the underlying idea is weak, the reward does not rescue it.

What is restaking, and does it change the choice?

Restaking means using already staked ETH, or a token representing it, to help secure additional decentralized services in return for extra rewards. It is described as extending staked ETH security to other services and explicitly says it can put staked ETH at more risk.

For cautious users, restaking is not where you begin. It adds another reward stream, but it also adds another risk surface. If plain staking already feels abstract, restaking is a sign to slow down, not speed up.

Where beginners get burned

The biggest mistakes are surprisingly consistent.

First, they compare APY before they compare failure modes. A prettier number is seductive. It also hides a lot.

Second, they forget that not all yield is the same kind of yield. Staking rewards come from protocol economics. Lending interest comes from borrowers and platform structure. Treating them as interchangeable is how people walk into risk they never meant to buy.

Third, they underestimate lockups. Liquidity feels boring until you need it.

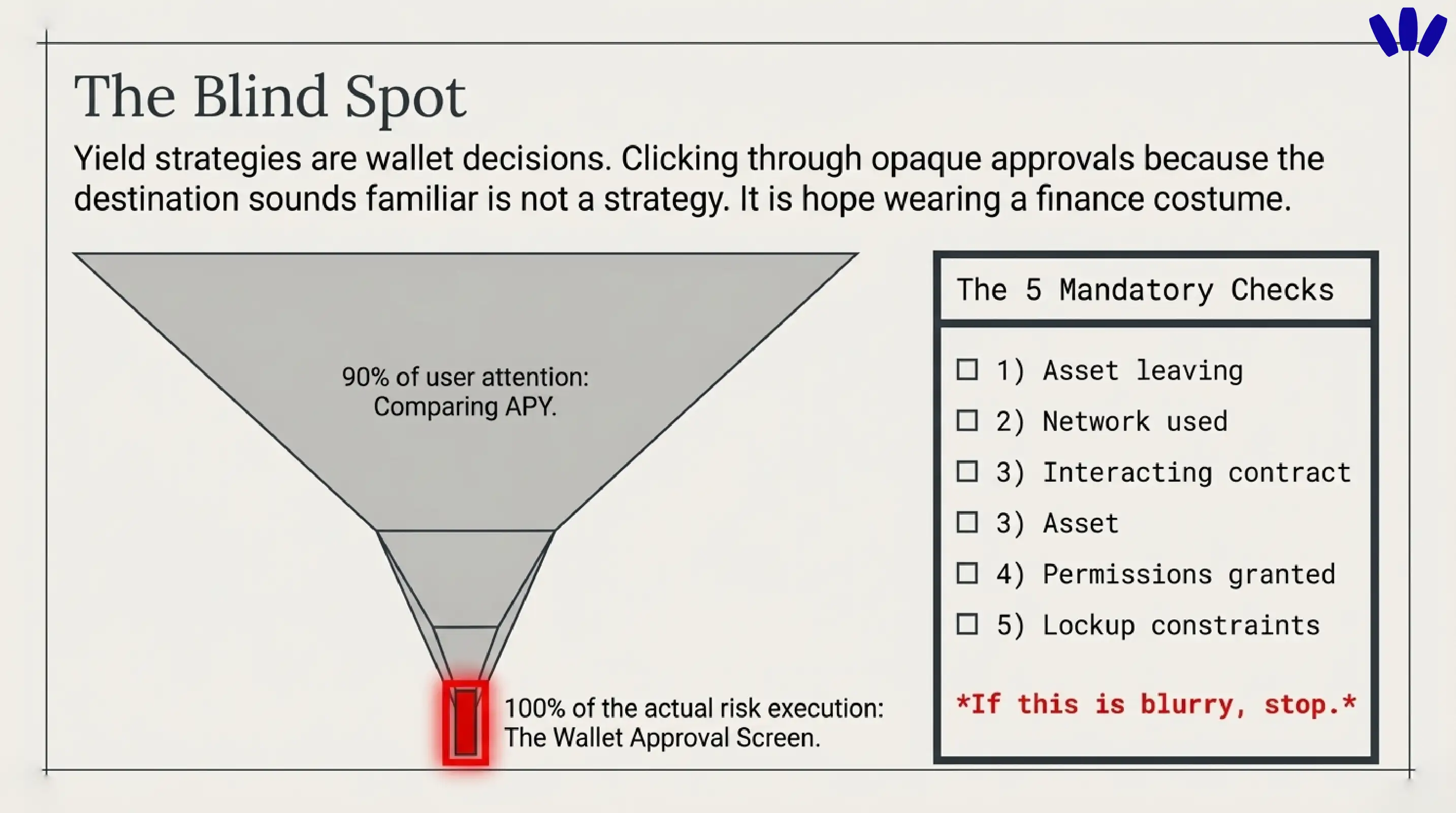

Fourth, they use a wallet or app flow they do not really understand. They click through approvals because the destination sounds familiar. That is not a yield strategy. That is hope wearing a finance costume.

What your wallet should show before you commit

This is the part most comparison articles skip, and it is exactly where a modern wallet can protect you from dumb but expensive mistakes.

Before you stake or lend anything, your wallet should make five things obvious:

what asset is leaving your wallet

what network you are using

what contract or app you are interacting with

what permissions you are granting

what you may not be able to undo quickly

If that is blurry, stop.

Reading approvals before you sign

A cautious user does not just ask, “What is the APY?” They ask, “What am I approving?”

That question matters more in lending and DeFi-adjacent flows because the real risk is often in the route, the approvals, and the contract exposure, not in the homepage headline. walllet’s legal and product language points toward this exact problem. Its terms are explicit that third-party dApps are independent, that users bear responsibility for the transactions they authorize, and that they should think carefully before approving transactions or interacting with smart contracts. At the same time, walllet consistently emphasizes human-readable transaction prompts, suspicious approval warnings, passkey-based access, and gas flexibility on supported flows.

That combination matters. A wallet cannot remove protocol risk. It can reduce user-error risk. And in yield strategies, user error loves to dress up as confidence.

walllet.com helps you read what is happening

Staking and lending are are wallet decisions.

If you are comparing two ways to put assets to work, you also need a wallet that helps you read what is happening at the moment of commitment. walllet’s public positioning is clear: it is a non-custodial smart wallet built around passkeys and ERC-4337, with credentials kept off walllet’s servers, biometric access, readable activity, and a broader product philosophy centered on making self-custody more understandable and less brittle. The homepage frames the product around hardware-level security, readable activity, and paying transaction fees with tokens you already own on supported flows. The terms spell out passkey-based authentication and the non-custodial model directly.

Related: Self-Custody vs Exchange for Everyday Crypto Use: Which One Makes More Sense?

That makes walllet especially relevant for readers in the cautious middle. Not the users chasing the highest yield in the weirdest corner of DeFi. The ones asking better questions. What am I signing? What am I exposing? Will I still understand this setup three weeks from now? What happens if I need out?

walllet is the layer that can make the risky moment more legible.

A softer next step makes sense here: see how walllet helps you read approvals and transaction details before you commit funds onchain. That is a better fit for this query than a hard sell, because readers at this stage are still deciding how to think, not just where to click.

So which one fits you?

If you already hold a proof-of-stake asset, plan to keep it for a while, and want the simpler mental model, staking is usually the more natural fit.

If you want yield on BTC or stablecoins, need more flexibility, or are intentionally taking platform and borrower risk in exchange for a different return profile, lending may fit better.

If you do not fully understand the route, the permissions, or the lockups, neither fits you yet.

And if your real problem is not “which earns more?” but “how do I stop making blind onchain decisions?”, walllet.com is a smart next step. Create your walllet with Face ID or fingerprint, explore a self-custodial wallet built to make crypto actions easier to read, and make your next staking or lending decision with less guesswork and more clarity.