Liquidation isn’t a mysterious market punishment. It is just the system’s way of saying your safety buffer is gone. Learn how liquidation works in DeFi lending and futures trading, what health factor means, why positions get liquidated, and how to reduce your risk with simple, beginner-friendly steps.

TL;DR

Liquidation in crypto means your position is forcibly closed because it is no longer safely backed.

In DeFi lending, liquidation usually happens when the value of your collateral falls too far relative to what you borrowed, and your position’s health factor drops below the protocol’s safety threshold. A health factor below 1 means the position becomes eligible for liquidation.

In futures trading, liquidation happens when your margin can no longer satisfy the exchange’s maintenance margin requirement, so the exchange closes some or all of your position.

The simplest way to avoid liquidation is to use less leverage, borrow less against volatile collateral, keep a big safety buffer, monitor your position, and act early instead of hoping the market turns around.

If you spend enough time around crypto, you start seeing the same word pop up everywhere: liquidation.

You see it in scary headlines. You hear traders say they “got liquidated.” You open a DeFi lending app and suddenly there is a number called “health factor” looking back at you like a quiet warning light on a dashboard.

For beginners, all of this can feel more dramatic than helpful.

So let’s make it simple.

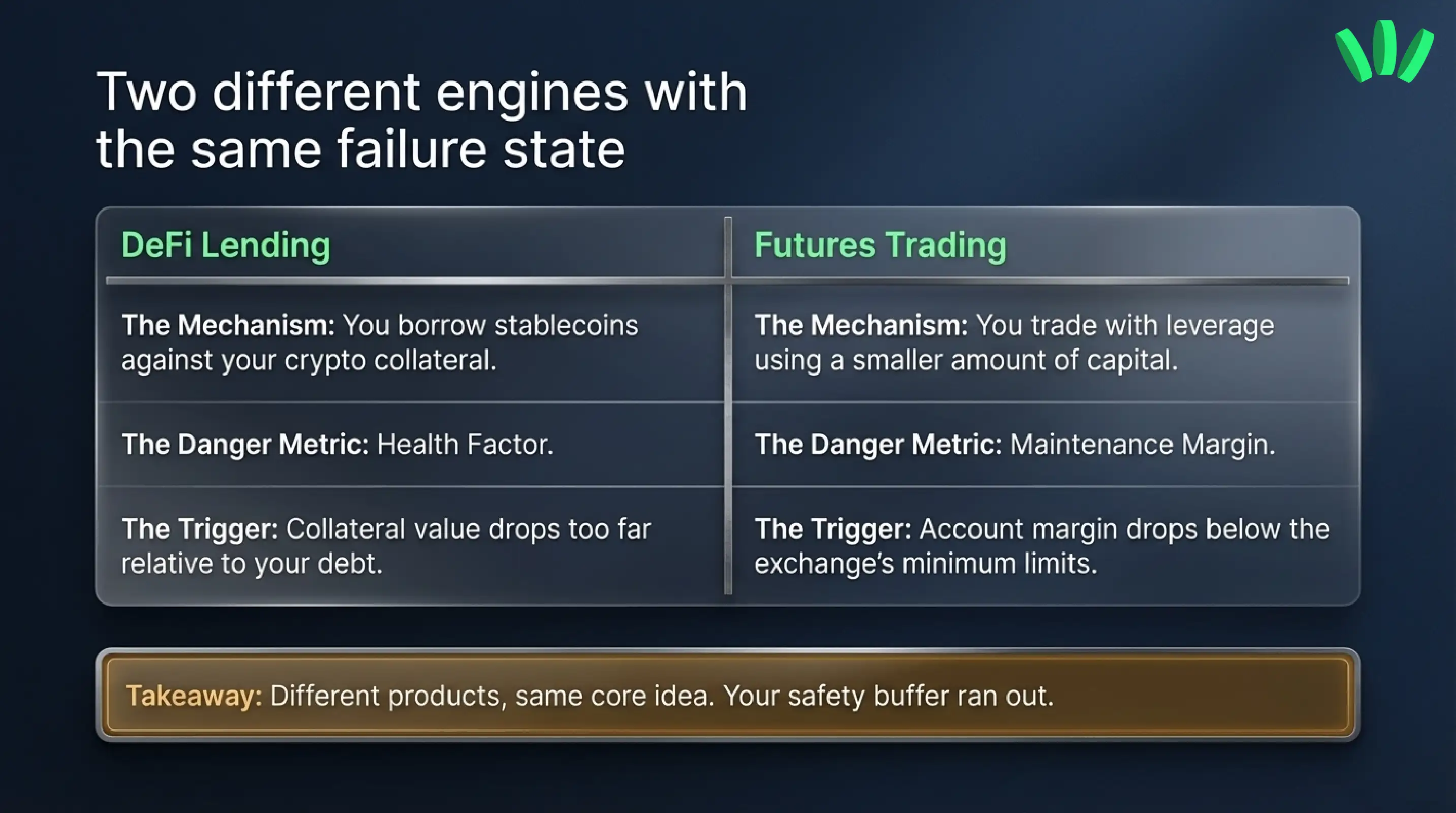

Liquidation is what happens when a platform decides your position is no longer safe enough to keep open. In DeFi, that usually means your collateral is no longer strong enough to back your loan. In futures, it means your margin is no longer enough to support your leveraged trade. Different products, same core idea: your buffer ran out.

This matters because liquidation is one of the most expensive ways to learn crypto risk. And unlike a simple price dip in a spot wallet, liquidation can lock in losses immediately.

First, what liquidation means

The easiest way to understand liquidation is to forget crypto for a second.

Imagine you borrow money and leave something valuable as collateral. The lender only agrees because that collateral is worth enough to protect them. If the collateral value drops too much, the lender cannot just wait around and hope for the best. They need a way to recover what they are owed.

That is liquidation.

Crypto systems do the same thing, just faster and more mechanically.

In DeFi lending, a smart contract watches whether your collateral still safely covers your debt. If it does not, the protocol allows liquidators to repay part of your debt and claim part of your collateral, usually with a bonus. In futures trading, the exchange monitors whether your margin still meets maintenance requirements. If it does not, the exchange closes your position before losses grow further.

Related: Sent Crypto on the Wrong Network? What You Can and Can’t Recover

So when people say “I got liquidated,” what they usually mean is one of two things:

1. Their DeFi loan became unsafe

They borrowed against crypto collateral, the collateral value dropped or the debt became riskier, and the protocol liquidated part or all of the position.

2. Their leveraged trade ran out of margin

They used leverage in futures or margin trading, the market moved against them, and the exchange forcibly closed the trade. Those are related ideas, but they are not the same product, and beginners often mix them up.

DeFi liquidation vs futures liquidation

This distinction is where many articles get fuzzy. It is better to keep it clean.

Aspect | DeFi Lending Liquidation | Futures Liquidation |

|---|---|---|

What you’re doing | Borrowing against crypto collateral | Trading a leveraged position |

What protects the platform | Your collateral | Your margin |

What usually triggers liquidation | Collateral value falls too much relative to your debt | Losses reduce your margin below maintenance requirements |

Main risk metric to watch | Health factor | Margin level / liquidation price |

What happens during liquidation | Part or all of your debt is repaid by a liquidator, who takes part of your collateral | The exchange forcibly closes part or all of your position |

Why it happens | Your loan is no longer safely backed | Your trade is no longer safely funded |

Beginner mistake | Borrowing too much against volatile collateral | Using too much leverage |

Safer beginner move | Borrow less, keep a bigger buffer, add collateral early | Use lower leverage, keep extra margin, cut risk sooner |

DeFi liquidation

Let’s say you deposit ETH as collateral and borrow a stablecoin against it.

This feels safe at first because you are not “selling” your ETH. You are just borrowing against it. But if ETH falls hard enough, your collateral-to-debt ratio gets worse. Once your position crosses the protocol’s liquidation threshold, it becomes eligible for liquidation. The health factor is the metric that expresses this safety, and a value below 1 means the position is eligible for liquidation.

This is why DeFi borrowers talk so much about health factor. It is basically your breathing room.

Futures liquidation

Now imagine something very different.

You open a BTC perpetual futures position with leverage. Instead of simply holding spot BTC, you are controlling a bigger position with a smaller amount of capital. That can amplify gains, but it also shrinks your margin for error. If the market moves against you and your account falls below maintenance margin, the exchange liquidates the position. It is the point where your funds no longer meet margin requirements, and a margin ratio of 100% triggers liquidation.

This is why liquidation in futures can happen so fast. High leverage turns small market moves into big account damage.

What is health factor?

If you only remember one DeFi term from this article, remember this one. Health factor is a number that tells you how safe your borrowed position is.

Health factor is the numeric representation of a borrow position’s safety, calculated from your collateral value, the liquidation thresholds of that collateral, and your total borrowed value. If it falls below 1, your position becomes eligible for liquidation.

You do not need to memorize the formula to use it well. You just need to understand the direction of travel.

If your collateral rises in value, your health factor usually improves.

If your collateral falls in value, your health factor usually worsens.

If you borrow more, your health factor usually worsens.

If you repay part of the debt or add more collateral, your health factor usually improves.

Think of it like this:

A health factor of 2 is not “twice as profitable.” It is simply safer than 1.2.

A health factor of 1.05 is not “basically fine.” It is standing on a banana peel.

That is the emotional trap for beginners. A position can feel okay right up until it really is not.

A step-by-step liquidation scenario for beginners

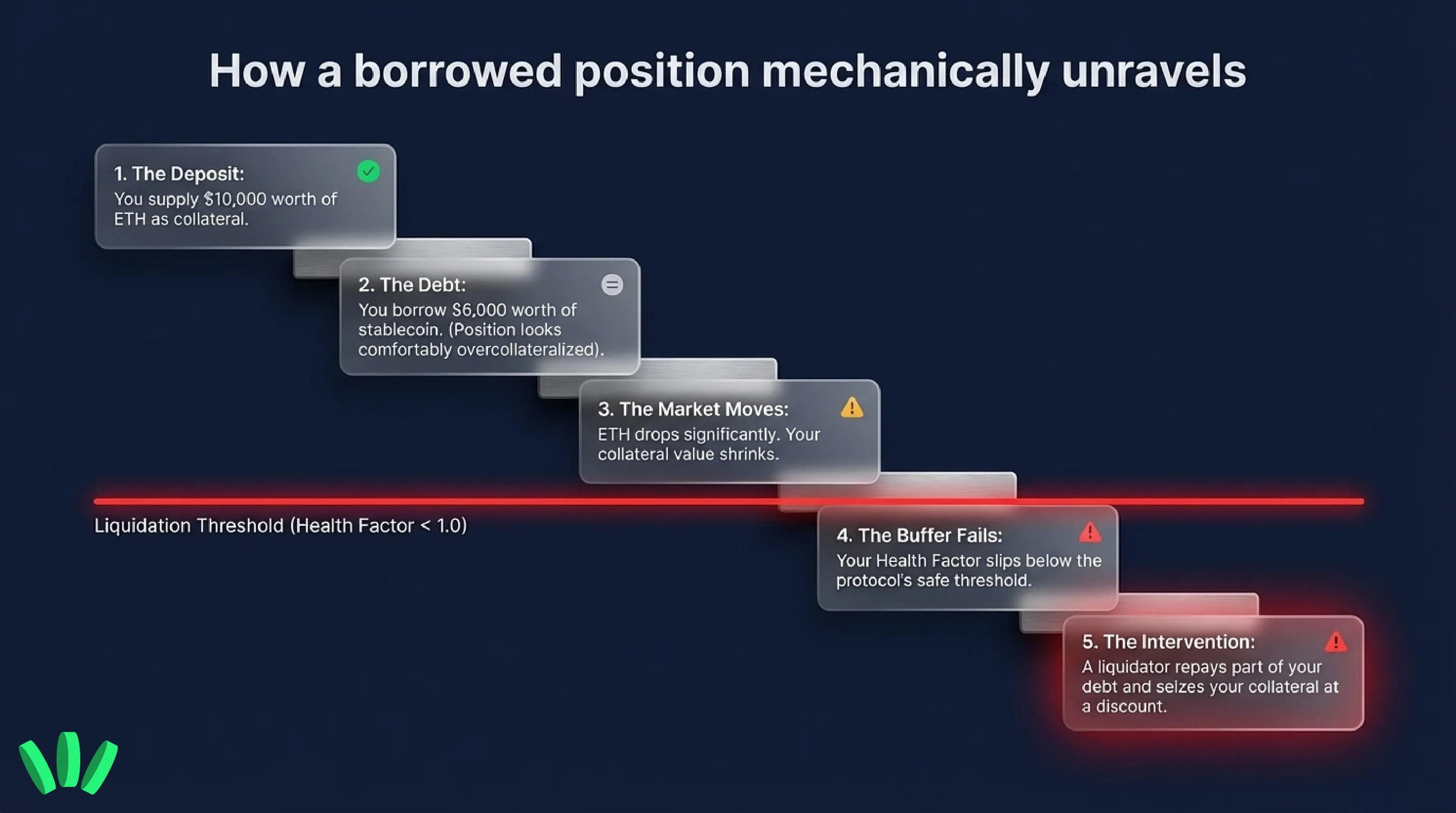

Here is the simplest possible DeFi example.

Step 1: You deposit collateral - You supply $10,000 worth of ETH to a lending protocol.

Step 2: You borrow against it - You borrow $6,000 worth of a stablecoin. At this moment, the position may look comfortably overcollateralized.

Step 3: The market moves - ETH drops. Now your collateral is worth much less than when you opened the loan.

Step 4: Your health factor falls - As collateral value shrinks, your buffer shrinks with it. If that health factor slips below the protocol’s safe threshold, liquidation can begin.

Step 5: A liquidator steps in - A liquidator repays part of your debt and receives some of your collateral, usually with a discount or bonus. The goal is not to punish you personally. The goal is to keep the protocol solvent.

Usually when the health factor is above 0.95 and both collateral and debt are at least $2,000, up to 50% of total debt can be liquidated. If the health factor is 0.95 or below, or if either side is below $2,000, up to 100% can be liquidated. That last part matters. Beginners often imagine liquidation as a clean, partial trim. In reality, once a position gets too unhealthy, the damage can become much more severe.

Why liquidation happens even if you plan to repay later

This is a common beginner question.

People say, “But I was going to repay the loan. Why liquidate me now?” Because the protocol or exchange does not judge your intentions. It only sees the risk in front of it.

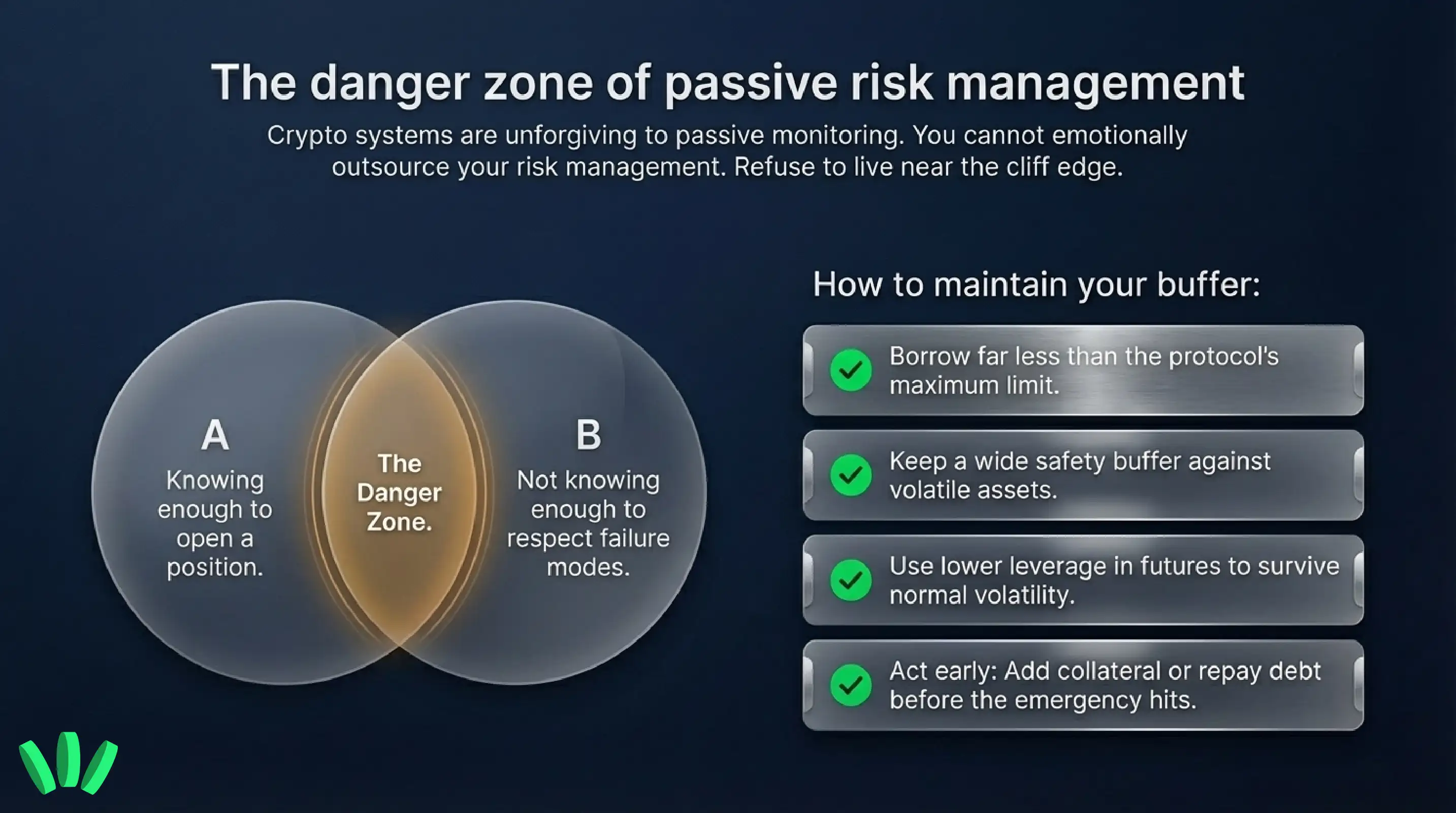

If collateral no longer safely covers debt, or if your margin no longer safely supports your trade, the system acts before the position becomes a bigger problem. That is why liquidation feels cold. It is rules first, feelings never. This is also why crypto is not forgiving to passive risk management. You cannot open a risky position and then emotionally outsource the monitoring part.

What you usually lose in a liquidation

Liquidation is not always the same as losing everything, but it is almost always worse than managing risk earlier yourself.

In DeFi, you may lose a chunk of your collateral at a discount. In futures, you may lose the margin backing the trade, and depending on product structure and jurisdiction, forced liquidation can be more expensive and less favorable than a normal exit. Liquidation can lead to worse execution than self-managed trades, and that losses can exceed the margin value in some cases.

The real cost is not just financial. It is behavioral.

A lot of people get liquidated not because they knew nothing, but because they knew just enough to open the position and not enough to respect its failure modes.

How to avoid liquidation

There is no magic trick here. Avoiding liquidation is mostly about refusing to live near the edge.

1. Borrow less than you technically can

The protocol may let you borrow up to a certain limit. That does not mean you should go anywhere near it. Beginners often treat maximum borrow capacity like a recommendation. It is not. It is the cliff edge.

2. Use lower leverage

In futures, lower leverage is one of the most direct ways to reduce liquidation risk because it gives your position more room to survive normal volatility. That is one of the clearest and most consistent risk-management points across exchange education materials.

3. Keep a real safety buffer

If your DeFi health factor is only slightly above 1, you are not “safe.” You are just not liquidated yet. Aave explicitly notes there is no universal safe health factor because safety depends on asset volatility and correlation, but the broad lesson is simple: thin buffers and volatile assets do not mix well.

4. Add collateral or repay early

Do not wait for the emergency.

If the market is moving against your collateral, act while you still have options. Adding collateral or repaying part of the loan improves health factor. Early intervention is the practical way to reduce liquidation risk.

5. Avoid borrowing against assets you barely understand

A volatile asset can be a great spot holding and still be terrible collateral for a loan. If you are new, correlated and relatively calmer positions are easier to manage than exotic collateral mixed with aggressive borrowing.

6. Set alerts and check your position on bad market days

You do not have to stare at charts all day, but if you borrow in DeFi or trade with leverage, you do need a habit. Open the dashboard. Check the number. Do not let the first warning be the liquidation itself.

walllet.com reduces product friction in this story

For a beginner, one of the biggest causes of bad DeFi decisions is mental overload. Too many tabs. Too many chain switches. Too many tiny balances scattered across too many apps. That clutter makes it easier to miss a risky position, harder to move funds calmly, and more likely that you make a rushed mistake when you need to act.

walllet.com’s current product and content positioning is already centered on simpler self-custody, integrated swaps, cross-chain movement, passkey-based onboarding, and a less fragmented DeFi experience. Its swap guide also states that walllet.com sponsors the network fee for swaps, does not add an extra walllet.com swap fee, and removes the need to keep native gas tokens just to complete a swap.

Related: Why Did My Swap Fail? 9 Reasons and Fixes (Slippage, Liquidity, Expiry)

Why does that matter in a liquidation article? Because reducing product friction helps users act earlier and think more clearly.

If you need to rebalance, swap into a safer asset, move funds between chains, or simplify your setup before opening a DeFi borrow position in the first place, a cleaner wallet experience helps. It doesn’t replace risk management, but it does reduce the chaos around it.

The honest framing is this:

walllet.com can make the surrounding workflow easier. It cannot make reckless borrowing safe. That is a good thing. Good crypto products should remove unnecessary friction, not hide necessary risk.

The beginner rule that saves the most money

Here is the rule in plain English: Do not open a position that would scare you during a normal bad day.

If a 15% to 20% market move would force you into panic, the position is too tight.

If checking your health factor feels stressful, the position is too tight.

If you need the market to behave perfectly for your plan to work, the position is too tight.

Crypto gives people a lot of tools. Liquidation is what happens when the risk tool starts using you back.

Final takeaway

Liquidation is a built-in safety mechanism for systems that involve borrowing, leverage, and volatile collateral. The mistake is entering products that can liquidate you without fully understanding what number, threshold, or price actually puts you in danger.

So if you are a beginner, keep the mental model simple:

Spot holding is one thing.

Borrowing is another.

Leverage is another again.

And the moment you step from simple holding into borrowed risk, your job changes. You are no longer just picking an asset. You are managing a position. Do that calmly, with room to breathe, and liquidation becomes a concept you understand instead of a lesson you pay for. Understand the risk first, then simplify the workflow. Use walllet.com to keep your assets, swaps, and cross-chain moves in one calmer place before you step into more advanced DeFi positions.