A stablecoin wallet can help people in high-inflation countries protect short-term purchasing power by holding dollar-pegged assets like USDT or USDC. But stablecoins are not risk-free savings accounts. A safer setup means choosing the right token, checking the network, using a wallet you can recover, starting small, and understanding depeg, issuer, custody, and regulatory risks.

TL;DR

Stablecoins can reduce exposure to a weakening local currency, especially when you need dollar-like value for savings, payments, or remittances.

They are not the same as money in a regulated bank account. Stablecoins can depeg, face issuer risk, be affected by regulation, or be lost through wallet mistakes.

The wallet matters because many everyday losses come from practical mistakes: wrong networks, lost access, phishing, unclear approvals, or keeping too much in one place.

The safest setup is usually simple: choose your purpose, choose the token, check the network, test a small transfer, and keep only a practical balance.

Your salary arrives. Rent is due. Groceries cost more than last month. The exchange rate moved again while you were sleeping.

That is the quiet panic behind many searches for stablecoins. People are not always looking for a “crypto opportunity.” Sometimes they are looking for a way to keep this month’s money from shrinking before next month begins.

Stablecoins can help with that. But only if you understand what they protect you from, what they do not protect you from, and how to hold them without turning a currency problem into a wallet problem.

If you are still learning the broader role of stablecoins, start with walllet’s guide to the best way to use stablecoins. This article focuses on one specific question: can a stablecoin wallet help you protect purchasing power in a high-inflation country?

Can stablecoins really protect against inflation?

Stablecoins can help protect purchasing power when your local currency is losing value against the dollar. Popular stablecoins like USDT and USDC are designed to track the value of the US dollar, which makes them useful for people who want dollar-like value without always relying on a local bank account, cash dealer, or international transfer service.

But a stablecoin is a crypto asset that tries to stay close to a target price, usually $1. If the peg weakens, if the issuer has problems, if your wallet is compromised, or if your country restricts stablecoin use, your “inflation hedge” can quickly become a different kind of risk.

The honest version is this: stablecoins can be useful for protecting short-term purchasing power, but they should be used with a careful wallet setup and a clear plan.

What are you really trying to protect?

Before choosing a stablecoin wallet, get specific about the problem.

You may be trying to protect next month’s expenses, freelance income, remittances from family, savings for a near-term purchase, or money you plan to spend or convert later. These are practical use cases. They are not the same as trying to “invest” in stablecoins.

A stablecoin does not usually grow just because you hold it. Its main job is to be more stable than volatile crypto assets like Bitcoin or ETH, and more dollar-like than a weakening local currency.

That matters because your setup should match the job. Emergency money, monthly spending money, and longer-term savings should not all sit in the same place with the same risk.

Stablecoin wallet vs exchange vs bank account

If you are using stablecoins to protect purchasing power, the question is not only “USDT or USDC?” It is also “where should I keep it?”

Option | What it helps with | Main risk | Best for |

Local currency cash | Daily spending | Inflation and depreciation | Immediate expenses |

Bank USD account | Regulated dollar access | Limited availability, fees, account restrictions | Users with reliable dollar banking |

Stablecoins on an exchange | Buying, selling, quick conversion | Custodial risk, account freezes, platform limits | Trading or short-term conversion |

Stablecoins in a self-custody wallet | Direct control and onchain use | User mistakes, lost access, scams, wrong networks | Holding and using digital dollars directly |

Stablecoin yield products | Potential return | Smart contract, liquidity, depeg, and custody risk | Advanced users who understand the risks |

A bank account may offer clearer legal protections, but many people in high-inflation countries do not have easy access to dollar banking. An exchange is convenient, but the platform controls the account layer. A self-custody wallet gives you direct control, but it also gives you direct responsibility.

If you are deciding whether funds belong on an exchange or in your own wallet, read walllet’s guide to self-custody vs exchange for everyday crypto use. The short version is simple: an exchange is useful for conversion, but a wallet is better when you want direct control.

Why stablecoins are popular in high-inflation countries

Stablecoins are useful because they can move across borders, settle on public blockchains, and hold dollar-like value without always depending on traditional correspondent banking.

The IMF says stablecoins could make cross-border payments faster and cheaper, especially where traditional systems are slow or costly. But the same analysis also warns about risks such as currency substitution, capital flow volatility, financial crime, and pressure on local banking systems.

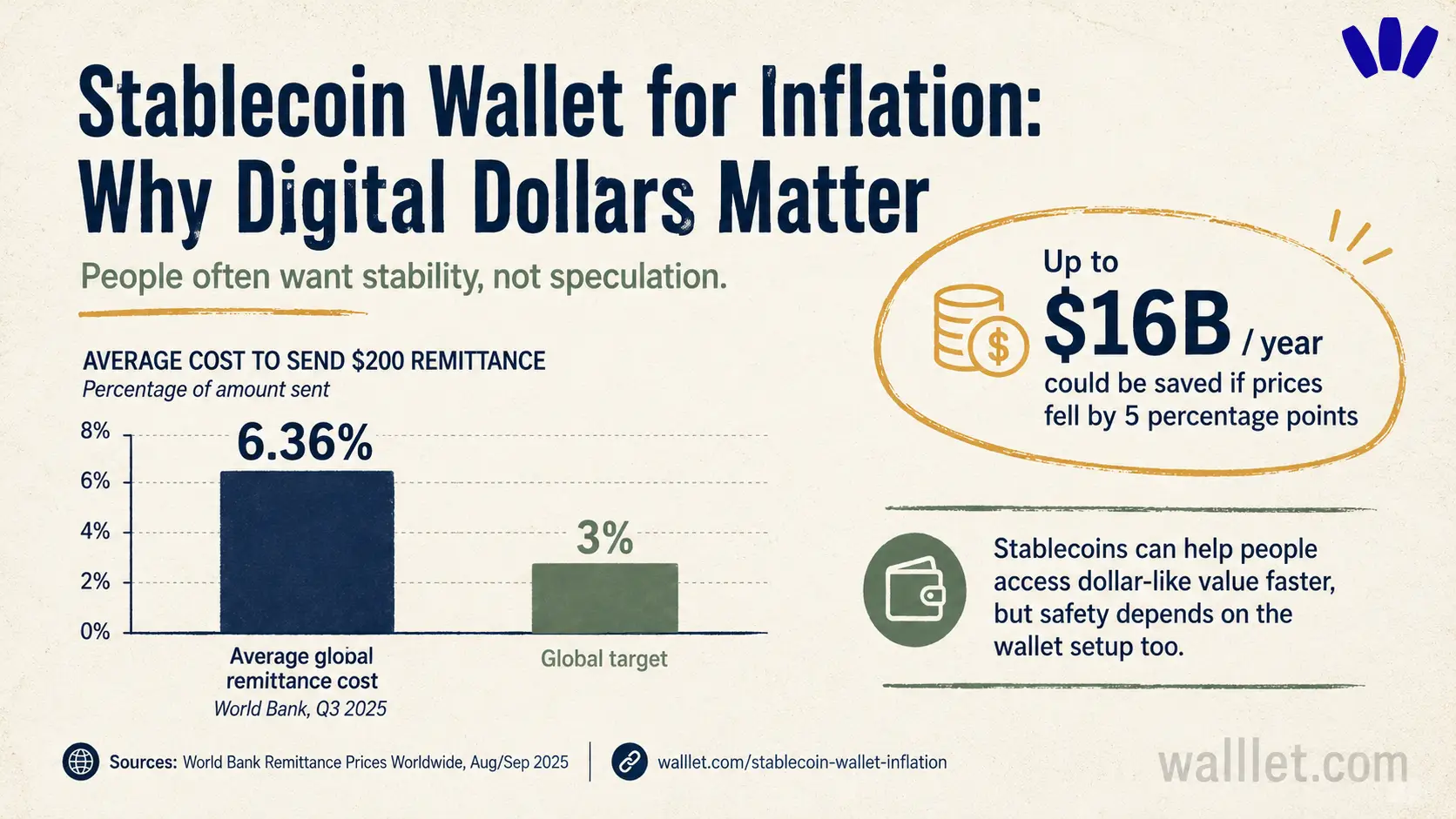

That tension is exactly why this topic needs nuance. Stablecoins are attractive because people have real problems with local currency, banking access, and remittance costs. The World Bank’s Remittance Prices Worldwide tracker reported that sending remittances globally costs an average of 6.36% of the amount sent.

So yes, stablecoins can make sense for people receiving international payments or trying to hold part of their income in dollar-like form. But popularity is not safety. How you hold, move, and recover those stablecoins matters just as much as the token itself.

What stablecoins protect you from, and what they do not

A stablecoin can help reduce exposure to a falling local currency. If your currency loses value quickly against the dollar, holding some USDT or USDC may keep your short-term purchasing power more predictable.

It can also help reduce exposure to crypto volatility. If you are paid in crypto or trade volatile assets, moving some value into a dollar-pegged stablecoin can reduce price swings.

But stablecoins do not protect you from everything. They do not remove issuer risk. They do not remove depeg risk. They do not remove regulatory risk. And they definitely do not remove wallet risk.

If you send funds to the wrong network, approve a malicious contract, lose access, or fall for fake support, the peg does not save you.

This is the point many stablecoin articles skip: inflation protection is about making the receiving, holding, checking, and spending flow safe enough for real people.

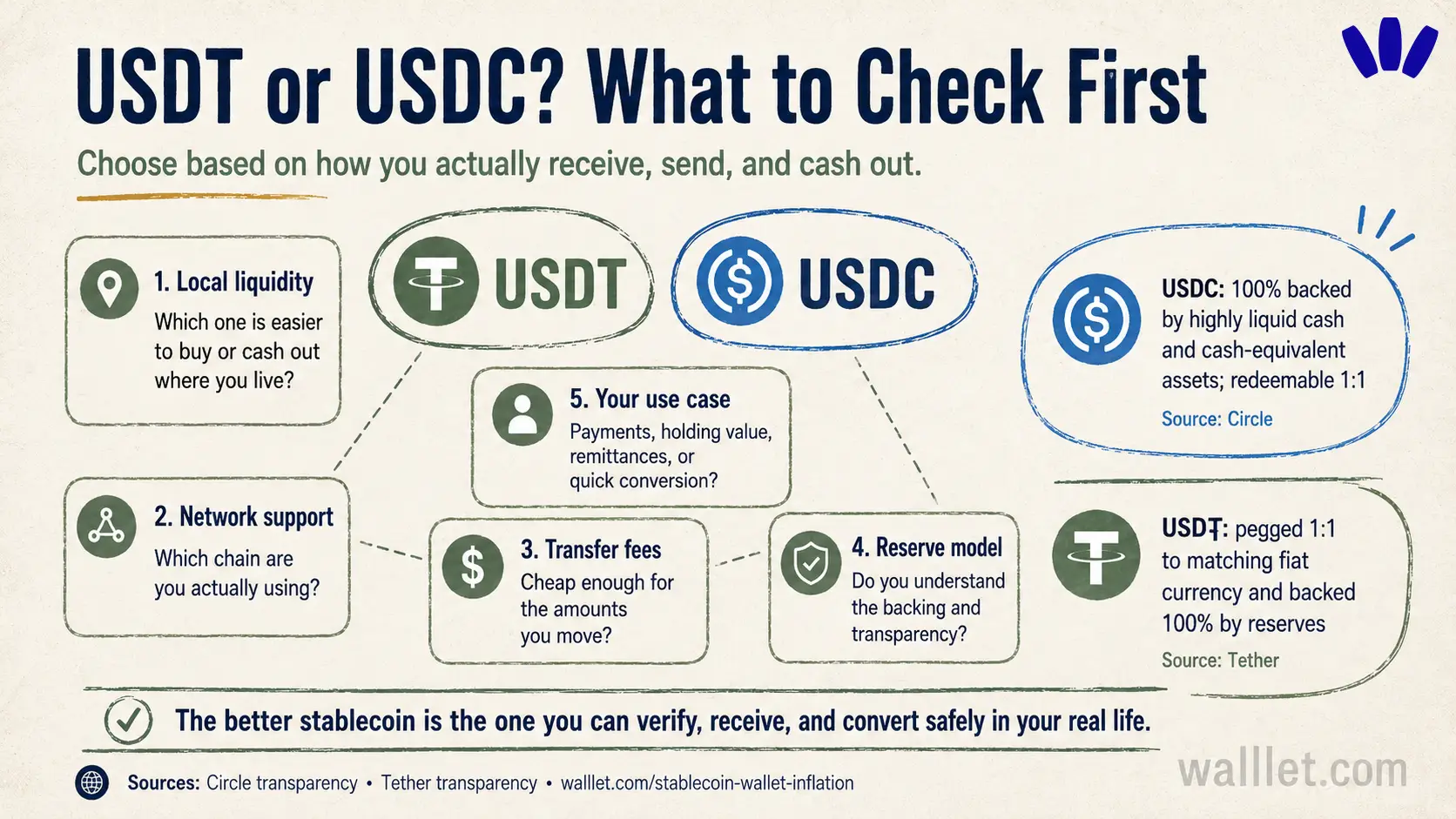

USDT or USDC: what should you check first?

Do not choose a stablecoin only because a friend uses it.

Before holding USDT, USDC, DAI, or any other stablecoin, check five things: liquidity, network support, fees, issuer model, and your actual use case.

For many everyday users, USDT may be more available locally, while USDC may appeal to users who care more about issuer transparency and reporting. That does not make either one universally better. The right choice depends on where you live, how you receive money, what networks you use, and how easily you can convert when needed.

If you want a deeper token-by-token comparison, read walllet’s guide to USDC vs USDT vs DAI. This article'real goal is to help you build a safer setup.

The network matters as much as the token

One of the most expensive stablecoin mistakes is thinking “USDT is USDT” or “USDC is USDC.”

Stablecoins exist on different blockchain networks. USDT on Ethereum is not the same transaction path as USDT on Tron, Arbitrum, BNB Chain, Polygon, or another network. USDC also exists across multiple chains. Sending the right token on the wrong network can create serious recovery problems.

A safer rule: always check the token, network, and receiving address before sending. Then send a small test amount first.

This is especially important when you are moving money under pressure. Urgency is where mistakes breed. The blockchain will not slow down and ask, “Are you sure this is the chain your wallet supports?” Your wallet experience has to help you catch that before the transaction leaves.

For a practical network decision guide, use walllet’s article on the best network to send USDT or USDC.

Why wallet setup matters more than people think

A weak wallet setup can ruin a good stablecoin plan.

Imagine someone receives $500 in USDC for freelance work. They wanted to protect that money from local currency depreciation. Then they save a seed phrase in a screenshot and lose access when their phone is stolen. Or they send USDT on a network their wallet does not support. Or they connect to a fake site that asks for a dangerous token approval.

None of those losses are “inflation.” They are wallet and custody problems.

That is why stablecoin users should treat wallet setup as part of the hedge. A stable asset inside a confusing wallet is only half a solution.

If phishing is one of your worries, walllet’s guide on how to avoid crypto phishing is a useful safety read before you start moving larger amounts.

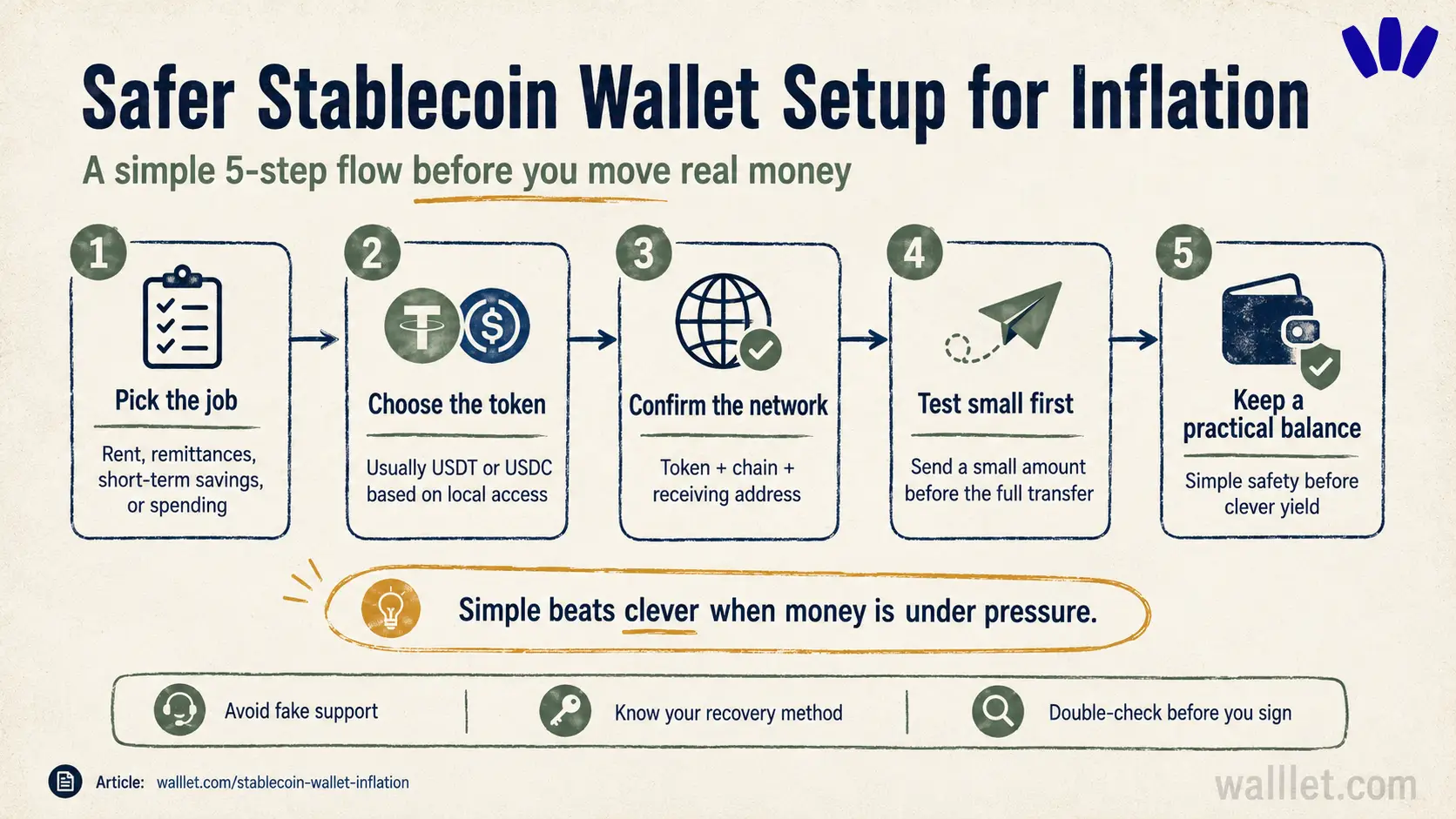

A safer stablecoin wallet setup for high-inflation countries

The best setup is usually boring. That is a compliment.

Start by deciding what the stablecoins are for. Are they for next month’s rent, emergency spending, freelance income, remittances, or future purchases? If the money is needed soon, prioritize liquidity and safety over yield.

Then choose the stablecoin based on access, not hype. Pick the token you can actually receive, send, convert, and understand. For many users, that means USDT or USDC.

Choose the network before you receive funds. Do not wait until someone is sending you money to figure out the chain. Confirm which networks your wallet supports, what fees look like, and whether the sender can use the same network.

Use a wallet you can operate under pressure. A wallet is not safe just because it looks clean. It is safer when the risky moments are understandable: receiving funds, checking networks, signing transactions, reviewing approvals, and recovering access.

Finally, test with a small amount first. Before receiving a full payment or moving savings, send a small test transaction. Confirm the wallet receives it correctly. Check the token and network. Make sure you understand how to access the wallet again.

A test transfer is not wasted time. It is cheap insurance.

Common mistakes when using stablecoins as an inflation hedge

The first mistake is treating stablecoins like a guaranteed savings account. They are not. They are crypto assets designed to maintain a peg, and that design can be stressed.

The second mistake is keeping too much in one stablecoin, one wallet, one exchange, or one network. If one part of the setup fails, concentration makes the damage larger.

The third mistake is chasing yield with money meant for safety. If the goal is protecting purchasing power, do not turn emergency funds into smart contract risk.

The fourth mistake is ignoring local rules. Stablecoin access can be affected by regulation, banking restrictions, exchange policies, and tax treatment. You should understand the rules where you live.

The fifth mistake is using a wallet you do not understand. If you cannot explain how to recover access, receive funds, check a network, and recognize a suspicious approval, you are not ready to move meaningful money.

How a seedless wallet can make stablecoin self-custody easier

For someone living in a high-inflation country, the hard part is rarely just “buy USDT.” The hard part is building a setup they can keep using safely: receive funds, check the token, avoid confusing signatures, manage access, and move money when needed.

A seedless wallet can help because it removes one of the most fragile parts of traditional self-custody: writing down a seed phrase and hoping future-you can find it during a crisis.

walllet.com is designed around this problem. It is a self-custodial, seedless wallet that uses passkeys and biometrics instead of a traditional seed phrase-first setup. For stablecoin users, that matters because the wallet should not add more anxiety to an already stressful money problem.

But seedless does not mean riskless. You still need to understand recovery, device security, transaction checks, and suspicious approvals. For that nuance, read walllet’s guide to seedless wallet risks.

The goal is not to pretend self-custody is effortless. The goal is to make the responsibility easier to understand and less brittle.

Is this safer than keeping money in a bank?

Not always. It depends on your country, your bank access, your currency, your legal protections, the stablecoin you use, and your wallet security.

A stablecoin wallet may give you easier access to dollar-like value and direct control. A bank may give you legal protections, customer support, and regulated account infrastructure. An exchange may give you easy conversion, but less direct control.

The safest answer for many people is not one tool. It is a balanced setup with clear jobs.

Need | Better fit |

Daily food, transport, rent | Local currency or local payment rails |

Quick buying and selling | Exchange |

Direct stablecoin holding and transfers | Self-custody wallet |

Long-term regulated savings | Bank or regulated financial account, where available |

Higher-risk earning strategies | Only for advanced users who understand the risks |

Stablecoins are a tool. A useful one. But tools still need handles.

Start small before moving serious money

Stablecoins can help people in high-inflation countries protect short-term purchasing power. They can make dollar-like value easier to receive, hold, send, and sometimes spend. That is meaningful when your local currency keeps losing ground.

But the protection is only as strong as the setup around it. Choose the token carefully. Check the network. Avoid yield traps. Understand the risks. Use a wallet you can recover and operate under pressure.

Create a seedless walllet and test it with a small USDT or USDC transfer before moving larger funds. Start small, confirm the token and network, and only move more when the flow feels clear.