Your card shows enough money.

The software subscription costs $49. You have $200 available. You click Pay.

Declined.

For freelancers and remote workers, especially those managing international income across Nigeria and similar markets, this can be more than a minor checkout problem. The card may be paying for your design software, cloud hosting, an AI subscription, a domain renewal, a business trip, or another tool you need to keep working.

The frustrating part is that the balance looks fine. But a balance is not an approval.

A crypto card or virtual dollar card can be declined even when you appear to have enough funds because card authorization depends on more than money. Billing details, merchant category, spending limits, country rules, provider controls, verification status, fraud checks, technical incidents, and the funding route behind the card can all affect whether the transaction is approved.

That distinction matters even more when your payment setup has several moving parts. You might:

get paid by a client in USDT or USDC,

receive it in a wallet,

move or swap it,

fund a card or card-linked balance,

pay an international merchant.

Each step can work individually while the final card payment still fails.

If you receive international income in stablecoins, start by understanding the full payment route and where freelancer payment risk can appear. The cheapest or most convenient-looking step is not enough. The route has to work from client payment to whatever you need to do with the money next.

The short answer: why can a card be declined despite sufficient balance?

A crypto card or virtual dollar card may be declined despite sufficient balance because the transaction still has to pass authorization checks. Depending on the card program and provider, those checks may include:

whether the billing information matches,

whether the merchant type is allowed,

whether the payment exceeds a per-transaction or daily limit,

whether the card can be used in that country or currency,

whether online, recurring, or international payments are enabled,

whether the transaction triggers a fraud or compliance review,

whether the card issuer, processor, or another provider in the route is experiencing an incident.

Official Stripe documentation on card declines describes several reasons legitimate payments can fail, including incorrect card data, issuer decisions, suspected fraud, and insufficient funds. The exact reason available to you depends on the card provider and how much of the issuer response it exposes.

So when a $49 transaction fails against a $200 balance, the useful question is:

“Which part of the authorization route rejected this payment?”

That is a much better troubleshooting question.

Why this problem matters for freelancers in Nigeria

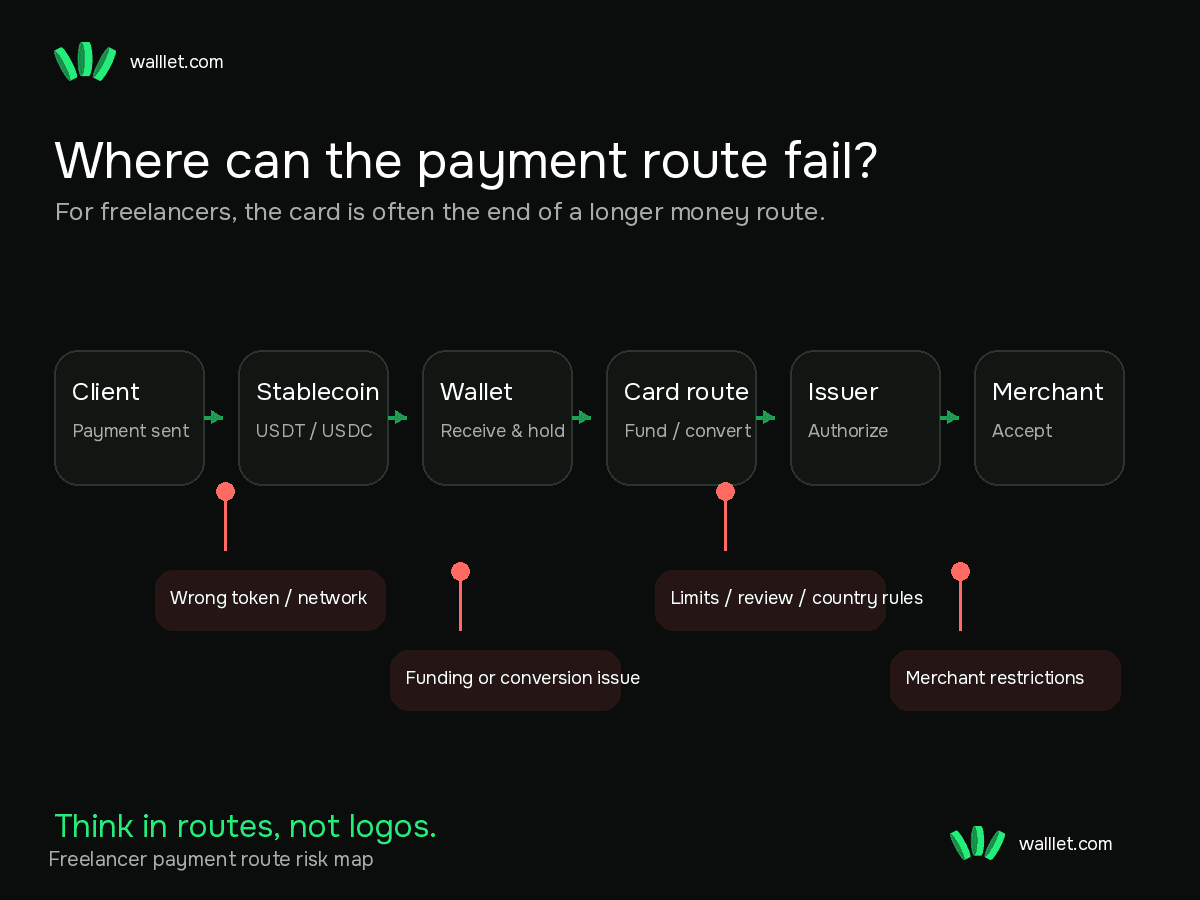

For many freelancers, the card is not the beginning of the money flow. It is the end. A realistic route might look like this:

International client → USDT or USDC → wallet → swap or funding step → virtual dollar card → foreign merchant

Another freelancer might use:

Marketplace payout → local account → card provider → USD card balance → SaaS subscription

Or:

Remote salary → stablecoin → wallet → supported spending route

Nigeria is especially relevant to this conversation because stablecoins already play a significant role in cross-border value movement. In June 2026, the IMF described Nigeria as a major stablecoin market and highlighted their growing use in cross-border transfers. But receiving digital dollars and successfully spending through a card are two separate problems.

A stablecoin can arrive correctly while the card transaction fails later. A card can be active while one merchant rejects it. A provider can show a balance while a transaction is blocked by a rule you never saw on the home screen. This is why freelancers should think in routes, not logos.

And before a client payment even enters that route, use a before-and-after stablecoin payment checklist to confirm the token, network, address, amount, test-payment rule, and transaction record. A broken incoming payment plus a broken spending route is a particularly ambitious way to ruin a Tuesday.

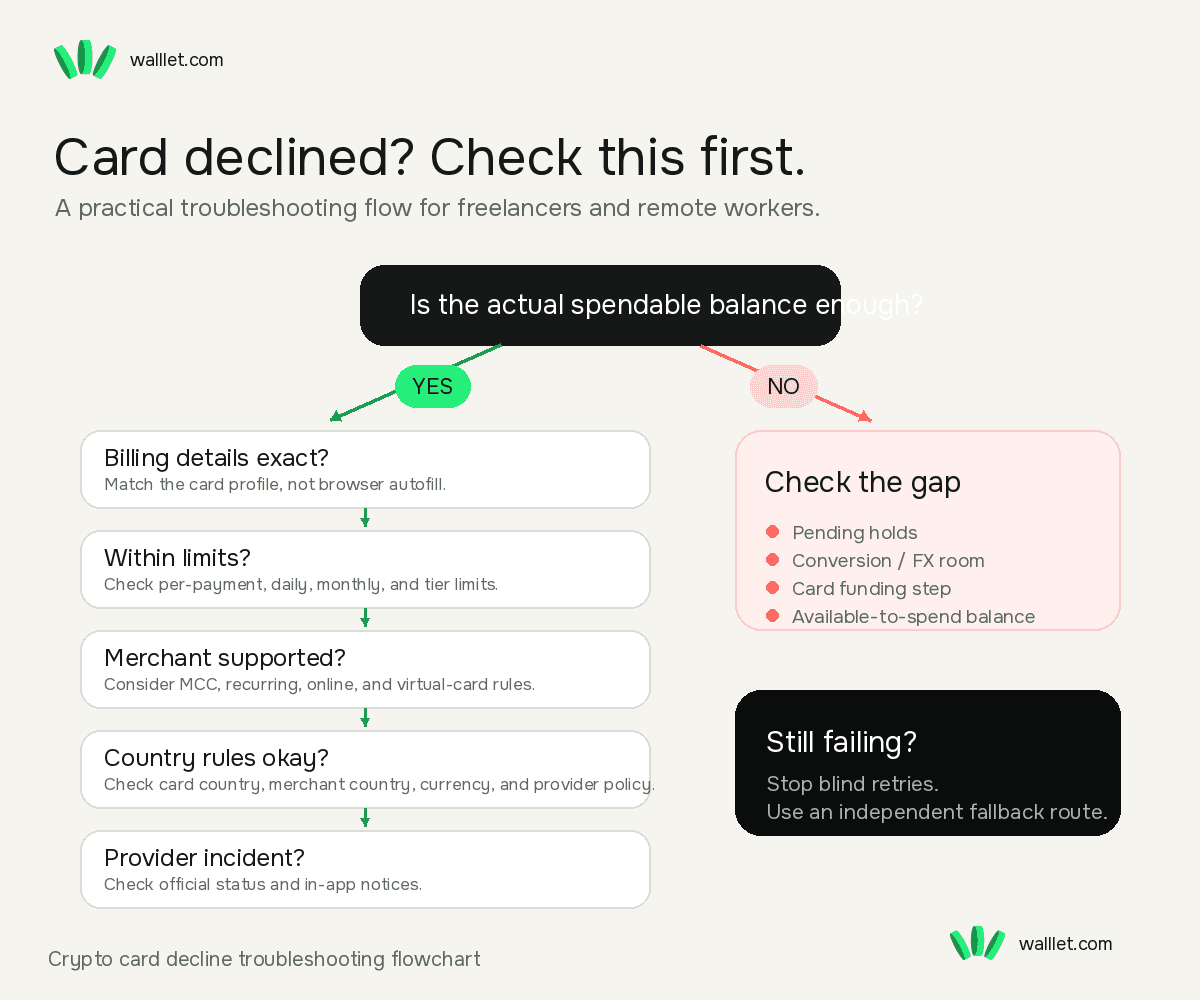

1. Enough balance does not mean enough spendable balance

Start here because the number on the screen can be misleading. Depending on how the card product works, you may be looking at one of several different balances:

crypto held in a wallet,

funds available in a card account,

funds already converted for spending,

funds reduced by pending authorizations,

funds subject to fees or FX conversion,

funds that are visible but temporarily unavailable for authorization.

These are not automatically the same thing.

Imagine you hold the equivalent of $120 in crypto and try to make a $118 purchase. The balance appears sufficient. But the payment route may also need room for conversion, exchange-rate movement, fees, or an authorization amount that differs from the final settled amount.

Hotels, car rentals, fuel stations, and some other merchants may also use authorization holds or estimated amounts rather than simply charging the final number you expect.

The practical rule is simple:

Do not compare only the purchase price with the headline balance. Check the card’s actual available-to-spend amount and any pending holds.

2. Billing address mismatch

A virtual card is still a card credential. The merchant may ask for: cardholder name, billing address, city, country, postal or ZIP code, CVV and expiry date. A common mistake is entering your home address because that feels logically correct while the card provider has a different billing address or country associated with the card profile.

For example: You live in Lagos, the merchant asks for a billing address, you enter your Lagos address, the card program expects the billing details stored in your card account. The payment may fail even though the card number and balance are correct. This is not universal. Merchants and processors handle address verification differently. Some barely use it. Others treat mismatched information as a meaningful risk signal. Before retrying, check:

What exact billing address does the card provider tell you to use?

Is the postal code correct?

Does the country match the card profile?

Did browser autofill insert an old address?

Is the cardholder name entered correctly?

Are you confusing your residential address with the card’s registered billing details?

One tiny autofill field can defeat an otherwise perfectly funded payment. Software remains deeply committed to comedy.

3. Merchant category restrictions

Cards do not necessarily work at every merchant just because they work on a major card network.

Merchants are classified by business type using merchant category codes, commonly called MCCs. Card issuers and card programs can apply controls based on those categories. Official card-issuing infrastructure can support merchant-category restrictions, spending controls, and geographic controls.

Depending on the provider, certain categories may be blocked or handled differently. Examples can include gambling, crypto purchases, money transfer services, financial services, cash-like transactions, adult services, certain subscriptions and specific high-risk merchant categories.

Do not assume this list applies to your card. Restrictions vary by provider. The important question is:

“Does this card support this type of merchant?”

For freelancers, this matters because two merchants that look similar to you may be classified differently in the payment system.

One software tool may work. Another subscription may fail. One advertising platform may accept the card. Another may not. The card is not making a philosophical judgment about your productivity. It is processing rules and risk signals.

4. Spending limits you did not notice

Virtual cards and crypto-linked cards may have more than one limit:

per transaction,

per day,

per week,

per month,

online spending,

international spending,

ATM withdrawal,

merchant-category-specific limits,

account-level limits,

limits tied to verification tier.

Suppose you have $1,000 available and attempt a $600 payment. The card can still decline if:

the per-transaction limit is $500,

you already spent most of your daily allowance,

a rolling limit has been reached,

your current verification level has a lower cap.

This becomes particularly annoying with freelancers because a normal work expense can be unusually large. Annual SaaS subscriptions, cloud credits, conference travel, advertising spend, laptops, and professional tools do not always resemble ordinary consumer spending patterns.

Before retrying, check the limit for the exact type of transaction you are making.

5. Country, currency, and provider rules

A card can be internationally branded without being universally usable. Several layers may matter:

your country of residence,

the country where the card was issued,

the merchant’s country,

the transaction currency,

the card provider’s geographic policy,

the merchant’s own acceptance policy,

the issuer or processor’s risk rules.

A freelancer in Nigeria might use a virtual dollar card to pay a US merchant. That sounds simple: dollar card, dollar merchant. But the transaction may still involve signals such as:

card issuance country,

billing country,

current IP location,

merchant country,

account profile,

device history,

previous spending behavior.

A mismatch is not automatically a problem. It can, however, contribute to a review or decline depending on the provider and merchant. Some merchants also refuse certain prepaid or virtual cards. Others may treat foreign-issued cards differently. Subscription businesses can have their own rules for recurring payments.

So “international card” should never be translated in your head as “works everywhere.” Marketing departments have inflicted enough damage already.

6. Verification or risk review

A card payment can be financially valid and still look unusual. Examples:

Your first large payment, several rapid attempts, a new merchant, a new country, an unusually high amount, a sudden change in spending behavior, a transaction that triggers additional authentication, an account that needs another verification step.

The result can be: an immediate decline, a temporary card restriction, a request for additional verification, a provider review, a transaction that works only after authentication. This is where repeated retries can make things worse.

If a payment fails once, do not automatically submit it ten more times in thirty seconds. First check the reason. Repeated attempts can look less like “persistent freelancer trying to renew Figma” and more like abnormal card activity. A controlled troubleshooting sequence is better than panic-clicking.

7. Provider incidents and infrastructure failures

Sometimes you did nothing wrong. The card is active. The balance is sufficient. The billing information is correct. The merchant is normally supported.

And the provider is having a bad day. A card payment can depend on several systems, which may include:

the card program,

issuer,

processor,

card network,

merchant acquirer,

fraud systems,

crypto conversion infrastructure,

internal funding systems.

The exact architecture varies by product. A failure or timeout in one part of the route can cause declines, delayed authorizations, or inconsistent behavior. This is why a card that worked yesterday can fail today without any visible change in your account. Before changing settings or moving money around, check:

the provider’s official status page,

in-app incident notices,

support announcements,

whether other transactions are failing,

whether the problem affects one merchant or every merchant.

One failed payment is a data point. Ten users reporting simultaneous failures is an incident.

The key realization: your card is one part of a route

This is the mistake worth fixing. Freelancers often evaluate each product separately:

Is this wallet good? Is this stablecoin cheap? Is this card convenient? Is this merchant international?

But your actual experience depends on whether the entire route works together.

For example:

Client sends USDT → you receive it → you swap it → you fund a card route → merchant authorizes the transaction

A problem at any stage can stop the final payment. That is why the right mental model is:

income route → holding route → conversion route → spending route → fallback route

If you want a simpler self-custodial place to manage supported crypto assets before deciding how to move or spend them, explore walllet.com

A wallet cannot force a merchant or card issuer to approve a payment. The useful part is having clearer control over the crypto side of your route instead of treating every step as one mysterious balance.

What to check before relying on a crypto card or virtual dollar card

Do this before the card becomes mission-critical.

Check | What to confirm | Why it matters |

Available spend | Actual spendable card balance, not only wallet balance | Visible crypto value may not equal available card funds |

Billing details | Exact address, country, postal code, and name expected by the card | Mismatched information can affect authorization |

Merchant support | Whether the merchant type is allowed | Some categories may be restricted |

Transaction limit | Per-payment cap | A large payment may exceed the limit |

Daily or monthly limit | Remaining allowance | Previous spending can reduce capacity |

International use | Countries and currencies supported | Cross-border transactions may face different rules |

Online payments | Card-not-present transactions enabled | A card may work differently online and offline |

Recurring payments | Subscription support | Initial and recurring charges may behave differently |

Authentication | Any required 3DS or verification step | Some payments need extra confirmation |

Pending holds | Existing authorizations | A hold can reduce available spending power |

Provider status | Current incidents or maintenance | A temporary outage can look like a card problem |

Fallback route | Another independent way to pay | Work should not stop because one card fails |

For freelancers who are still deciding how client income should arrive in the first place, compare PayPal, Payoneer, Wise, and stablecoins as different payment routes. The best receiving method is not automatically the best spending method.

A practical pre-reliance test for freelancers

Before trusting a card with a critical payment, test the actual use case. Do not merely activate the card and celebrate. Try the route you genuinely need.

If you use the card for SaaS

Check:

one small online purchase,

the exact billing address,

recurring payment support,

international merchant support,

what happens when the subscription renews.

If you use it for travel

Check:

airline purchases,

hotel authorization policies,

larger transaction limits,

foreign currency handling,

backup payment methods.

If you use it for business operations

Check:

cloud services,

advertising platforms,

software vendors,

annual subscriptions,

high-value purchases.

A successful $3 test at one merchant does not prove that a $700 annual software bill will work somewhere else.

Test the category, country, amount, and payment type you actually depend on.

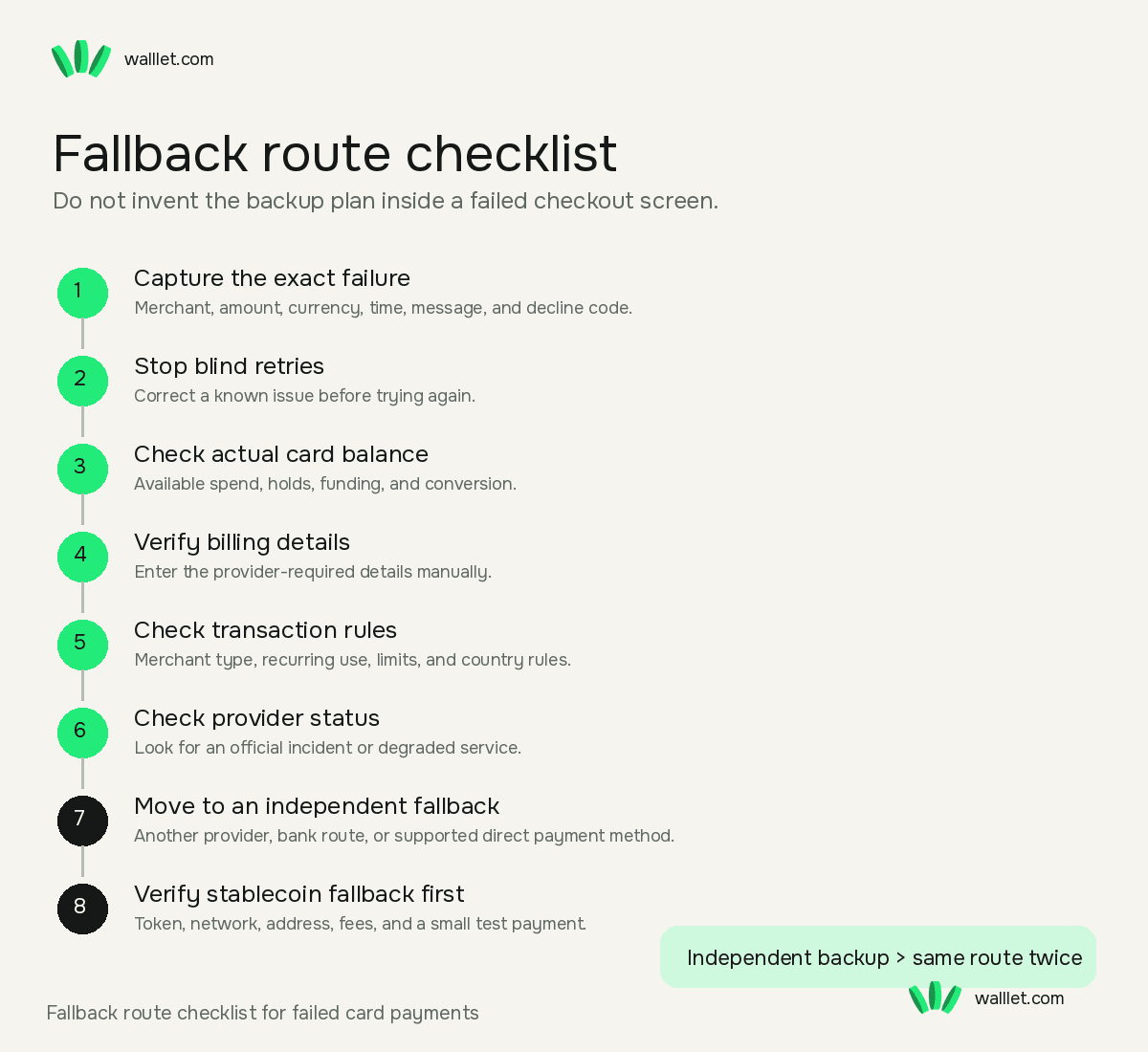

The fallback route checklist

A freelancer should not discover the fallback plan while standing inside a failed checkout screen. Use this sequence.

1. Capture the exact failure

Save: merchant name, amount, currency, date and time, decline message, provider decline code, if shown. “Card failed” is too vague to troubleshoot.

2. Stop blind retries

One retry after correcting a clear mistake can make sense. Repeated retries without changing anything usually do not. First identify whether the issue is: billing data, limit, merchant restriction, verification, insufficient available spend, country rule, provider incident.

3. Check the actual card balance

Confirm: available-to-spend balance, pending transactions, authorization holds, required funding or conversion step. Do not rely only on the total crypto value visible somewhere else in the app.

4. Verify billing information manually

Turn off the little chaos machine known as browser autofill for a moment. Re-enter: cardholder name, billing address, city, postal code, country, CVV and expiry date. Use the details required by the card provider.

5. Check merchant and transaction rules

Ask:

Is this merchant category supported?

Is this a recurring transaction?

Is the card accepted for subscriptions?

Is the merchant foreign?

Is the amount above a limit?

Does the merchant accept virtual or prepaid cards?

6. Check for a provider incident

Look for: status page updates, in-app banners, official support posts or recent incident reports. Do this before dismantling your entire payment setup because one processor is temporarily sulking.

7. Move to an independent fallback

Your fallback might be:

another card from a genuinely different provider,

a bank transfer,

a supported local payment route,

direct stablecoin payment when the recipient accepts it,

another invoicing or payout method.

The word independent matters. Two cards can look like separate products while depending on the same underlying issuer or processing infrastructure. If your backup depends on the same failing layer, it is decoration, not redundancy.

8. If stablecoins are the fallback, verify the route first

Do not respond to a card failure by rushing into a crypto transfer. Check:

exact token, exact network, receiving wallet support, destination address, fees, test amount and transaction record.

Use the guide to choosing the right network for USDT or USDC before moving funds, especially when a recipient supports only one chain. And remember that stablecoins introduce their own risks. Before treating USDT or USDC as a risk-free fallback, understand how stablecoin freeze and issuer controls can work.

9. Verify incoming crypto before spending against it

If your fallback depends on a client payment or transfer that just arrived, do not rely on a screenshot. Confirm:

transaction status,

token,

network,

amount,

receiving address.

This guide explains how to verify a crypto transaction on a block explorer. The fallback should reduce uncertainty, not move it to a different screen.

A better setup for freelancers: separate primary, backup, and emergency routes

The strongest setup is rarely one perfect card. It is a small payment system you understand. A practical structure can look like this: Primary route:

The method you normally use for routine subscriptions and business expenses.

Backup route: A genuinely separate payment method that can take over when the primary route fails.

Emergency route: A method reserved for critical expenses such as internet, hosting, travel, or essential work tools.

For a Nigerian freelancer, that might mean using different combinations of: a stablecoin wallet, a virtual dollar card, another independent card, local bank rails, direct client payment methods. The exact combination depends on your work, clients, providers, and local availability. The principle is more important than the product list:

Do not let one card become a single point of failure for your income-producing work.

Save this checklist before your next important payment

Before relying on a crypto card or virtual dollar card, check:

Is the card active?

Is the amount actually available to spend?

Are there pending holds?

Is the billing address exact?

Is the postal code correct?

Is the merchant category supported?

Is the payment below the per-transaction limit?

Is there enough daily or monthly allowance left?

Are international payments supported?

Is the merchant country allowed?

Are recurring payments supported?

Is extra authentication required?

Is the account under review?

Is the provider reporting an incident?

Do I have an independent fallback route?

The bigger lesson is simple.

A balance tells you how much value you have. It does not tell you whether this merchant, through this route, under these rules, will receive an approval.

For freelancers and remote workers, that difference matters because the card may sit between you and the tools you need to earn. So do not build your payment setup around the assumption that one funded card will always work.

Build it around route visibility, tested limits, known billing details, and a fallback that you have already checked. Try walllet.com if you want a simpler self-custodial way to manage supported crypto assets before choosing how to move, hold, or use them.

walllet cannot make a card issuer approve every transaction. No wallet can. The point is to make the crypto side of your money route easier to understand and control before the next payment decision.