Sending money home should not feel like a technical exam where one wrong network, wallet, or address can put the whole transfer at risk.

Stablecoin remittances let migrant workers send digital dollars such as USDT or USDC to family members through a crypto wallet. They can be faster and more flexible than traditional transfers, but safety depends on choosing the right stablecoin, network, wallet, address, and cash-out path before sending meaningful money.

TL;DR

Stablecoins can help migrant workers send digital dollar value to family members, often with faster settlement than traditional money transfer routes.

The wallet experience matters as much as the stablecoin, especially when the person receiving the money is not used to crypto.

The real cost is not only the blockchain fee. It can include exchange spreads, on-ramp fees, off-ramp fees, and local cash-out costs.

The biggest mistakes are wrong network, wrong address, weak wallet security, and unclear local cash-out.

Start with a small test transfer before sending anything important.

A worker sends money home every month. Maybe it is for rent, school fees, medicine, groceries, or a younger sibling’s phone bill. The amount might look small on a banking screen, but at home it carries the weight of a whole week.

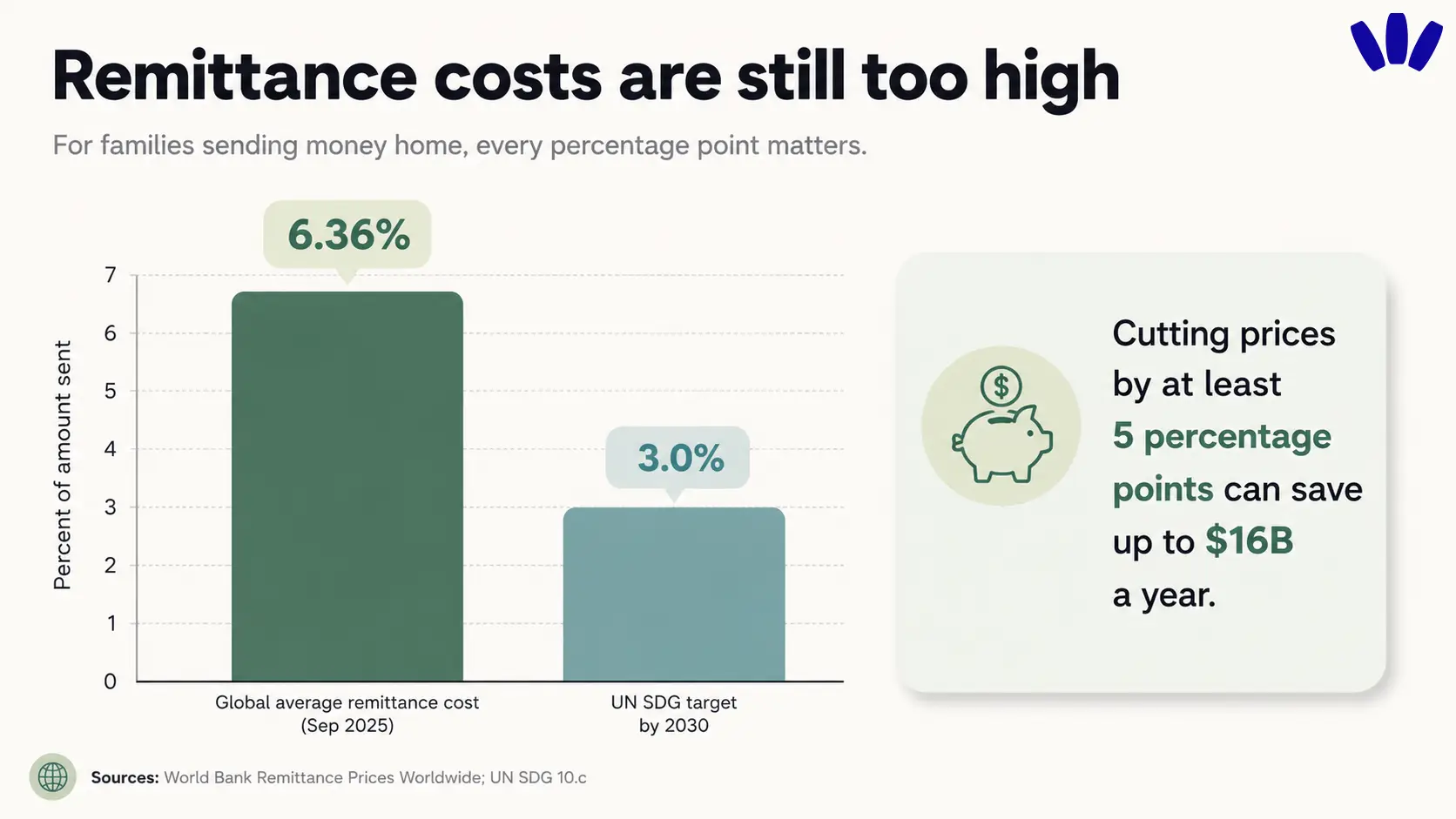

That is why remittance fees hurt. According to the World Bank’s Remittance Prices Worldwide database, sending remittances globally costs an average of 6.36% of the amount sent. For someone sending money every month, that is money that could have reached the family.

Stablecoins are one reason migrant workers are looking for another route. If you are new to the idea, start with this plain-English guide to USDC, USDT, and DAI. The short version is this: stablecoins can move value across borders quickly, but the full journey still needs care. You need the right stablecoin, the right network, the right wallet, and a clear plan for how the family will use or convert the money.

Stablecoins are useful when they make family money easier to receive and understand. They become risky when people treat “fast” as the same thing as “safe.”

What is a stablecoin remittance?

A stablecoin remittance is a cross-border transfer where the sender uses a stablecoin, usually a digital asset linked to a currency such as the US dollar, to send value to another person’s crypto wallet.

The Bank of England describes stablecoins as digital assets designed for payments and usually backed by assets such as a country’s currency. It also mentions cross-border payments, including sending money to family or friends in another country, as one use case.

For migrant workers, the basic flow is simple: the sender gets USDT or USDC, the family member shares a wallet address, the sender chooses the correct network, and the recipient receives the stablecoin.

The danger is hidden inside the “simple” part. USDT on one network is not always the same practical transfer route as USDT on another network. Before sending, check this guide on the best network for USDT or USDC, because network choice is one of the easiest places to make a painful mistake.

Stablecoin remittances vs traditional money transfers

Here is the practical difference. Not the glossy version, the kitchen-table version.

Option | Best for | Main strength | Main risk | What to check first |

Bank transfer | Formal bank-to-bank transfers | Familiar and regulated | Slow delivery, fees, FX spreads | Total cost and arrival time |

Money transfer operator | Cash pickup or family support | Local payout network | Transfer fee and exchange-rate margin | Recipient location and payout method |

Mobile money | Mobile-first countries | Familiar for recipients | Corridor availability | Whether sender and receiver are supported |

Stablecoin transfer | Wallet-to-wallet digital value | 24/7 movement across borders | Wrong network, wrong address, cash-out friction | Stablecoin, wallet, network, and off-ramp |

Self-custodial wallet | Receiving and holding stablecoins | User keeps control of funds | User must understand security and recovery | Wallet access, supported assets, and backup model |

The important point is this: a stablecoin transfer is only one part of the remittance route. If your family cannot cash out, spend, or confidently hold the stablecoin, the transfer may be fast but still not useful.

Why migrant workers are looking at stablecoins

Traditional remittances can be expensive, slow, and hard to compare. The visible fee is only one part of the cost. The exchange rate, payout method, receiving country, local provider, and delivery speed all matter.

Stablecoins offer a different path because they can move on public blockchain networks around the clock. That can be useful for migrant workers who send money outside banking hours, across difficult corridors, or to family members who need faster access to value.

But the better question is:

Can this specific sender and this specific family receive, understand, use, and recover access to the money safely?

That is where many generic crypto guides go thin. They explain the rail, then skip the family reality. A mother, spouse, sibling, or parent does not care that a payment settled onchain. They care whether the money arrived, whether it is still close to the amount expected, and whether they can use it without asking five people for help.

How sending money home with stablecoins usually works

The sender first needs USDT or USDC. This may happen through an exchange, wallet provider, on-ramp, employer payment, P2P marketplace, or another compliant local route.

Then the recipient needs a wallet that supports the stablecoin and the network being used. A wallet address is not a bank account number. It is public, long, unforgiving, and usually network-specific. If the family member copies the wrong address, uses the wrong chain, or trusts a fake support account, the transfer can become difficult or impossible to recover.

For safe transfer habits, it is worth reading this step-by-step guide on how to send and receive ETH and ERC-20 tokens safely. Even if you are sending stablecoins, the habits are similar: copy carefully, check the address, confirm the network, and test before sending more.

Once the family receives the stablecoin, the next question is what they will do with it. Will they hold it? Convert it to local currency? Spend it online? Move it to another wallet or exchange? Need native gas to move it again?

Receiving the stablecoin is not the finish line. The finish line is the family being able to use the value safely.

Best crypto wallet for stablecoin remittances: what families should check

For stablecoin remittances, the best wallet is the one the sender and recipient can actually understand under pressure.

A good wallet for family stablecoin transfers should help with four things: clear receiving, clear network support, secure access, and understandable transactions. This matters because the sender may be comfortable with crypto, while the family member receiving the money may not be.

This is where walllet.com can be useful. walllet is a self-custodial, seedless smart wallet built to reduce seed phrase friction while keeping users in control of their funds. Its setup uses passkeys and biometrics, so users do not have to start by writing down a fragile recovery phrase. You can read more in this guide to what walllet.com is and how its seedless smart wallet works.

For migrant families, that product choice matters because wallet anxiety is real. A family member may not understand private keys, gas tokens, or chain names. They may just want to know: “Did the money arrive? Can I use it? Am I about to press something dangerous?”

walllet.com should not be treated as a bank, money transfer company, or guaranteed cash-out provider. Its role is the wallet layer: helping users receive, hold, review, and move supported crypto with less seed phrase stress and clearer transaction understanding.

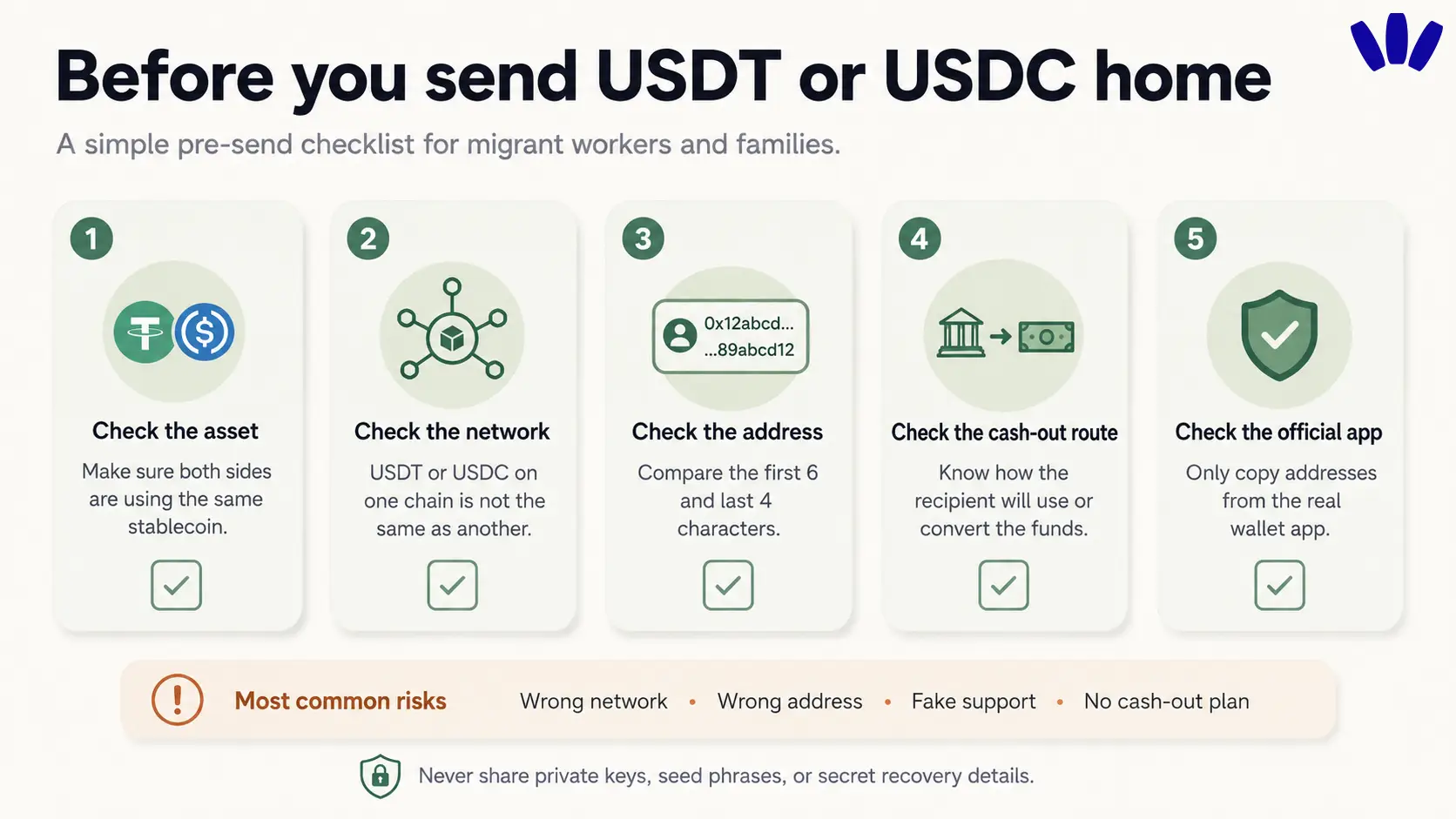

Safety checklist before sending stablecoins to family

Before sending anything meaningful, slow down. Most expensive crypto mistakes happen when someone rushes.

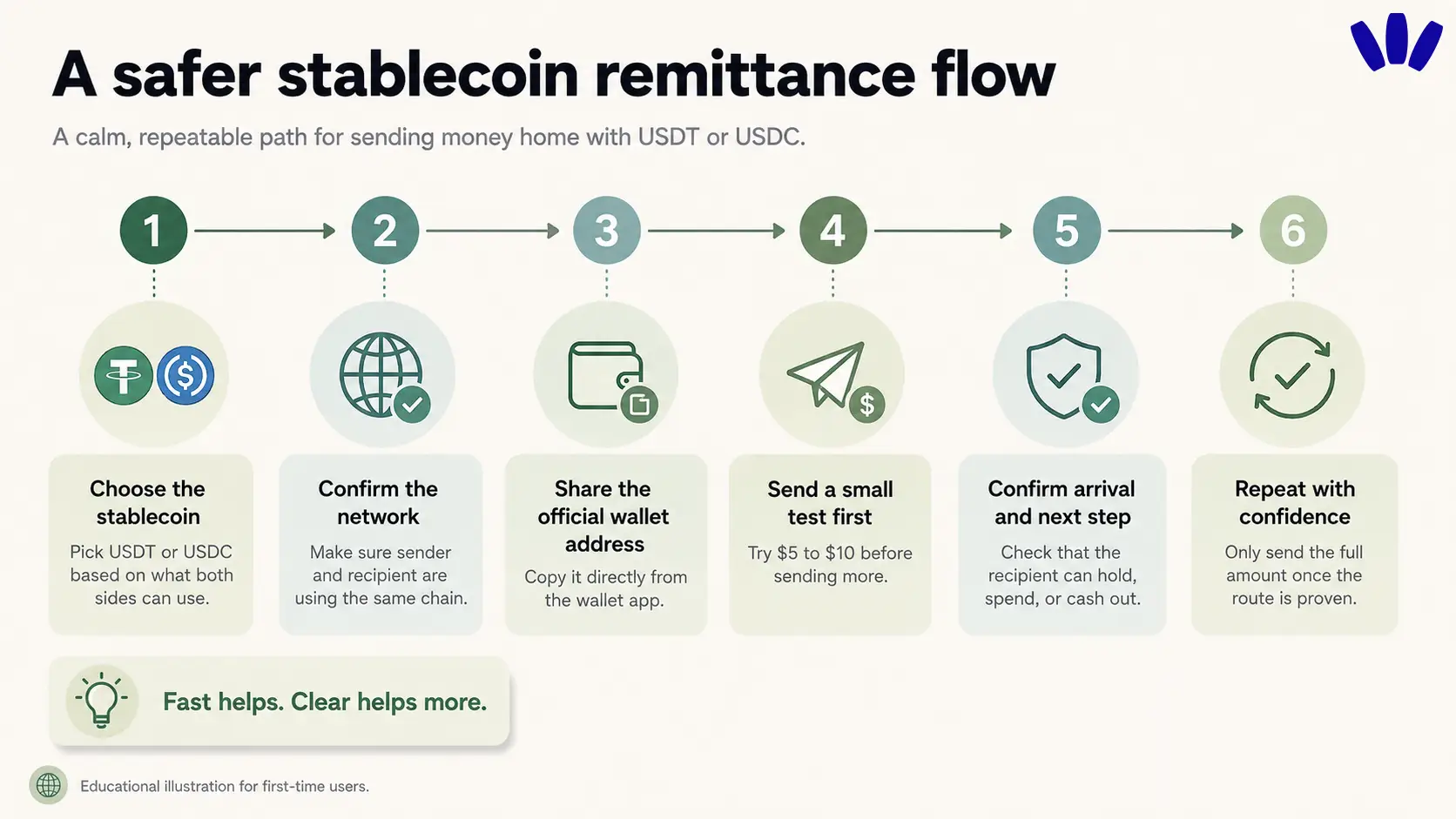

Confirm the recipient wallet supports the stablecoin. Confirm the exact network, not just the token name. Copy the address from the official wallet app and check the first 6 and last 4 characters. Send a small test amount first, then wait until the recipient sees it.

Before repeating the transfer, make sure the family knows what they can do next. Can they hold it? Convert it? Spend it? Send it back if needed? Do they understand which app is official?

Also, never trust random “support” accounts in DMs. A real wallet or exchange should never ask for your private key, seed phrase, passkey credentials, or secret recovery details.

A small test transfer is a rehearsal. A $5 test can protect a $500 mistake.

What can go wrong?

The most common problem is the wrong network. The sender chooses one network, the recipient expects another, and the money does not show up where expected. Sometimes it can be recovered. Sometimes it cannot. Either way, it creates stress at the exact moment the family expected relief.

The second problem is the wrong address. Crypto transfers are usually final. If you send to the wrong address, there may be no bank-style reversal.

The third problem is fake support. Scammers know that confused users panic. They create fake Telegram, WhatsApp, X, or email support accounts and ask for secret details.

The fourth problem is cash-out. A family might receive USDC successfully but still struggle to convert it locally. This is why stablecoin remittances should be planned as a full route, not a single send button.

And finally, stablecoins themselves carry risk. They are designed to stay close to a reference value, usually the US dollar, but they are not the same as insured bank deposits. Issuer risk, depeg risk, regulatory changes, and liquidity issues can all matter.

Is USDT or USDC better for sending money home?

There is no universal answer.

USDT often has broad liquidity and strong availability in many markets. USDC is often preferred by users who care about transparency posture and regulated issuer framing. But the right choice depends on where the sender is, where the recipient is, which networks are supported, and how the family plans to use or convert the money.

For a family transfer, the practical question is:

Which stablecoin can both sides receive, verify, and use with the least confusion?

If the recipient’s local cash-out route supports USDT but not USDC, that matters. If the wallet supports USDC on one network but the sender chooses another, that matters too.

How to test a stablecoin remittance before sending more

The safest first transfer is not the real transfer. It is a test.

Ask the recipient to create a wallet and open Receive. They should share the address from the official wallet app, not from a screenshot passed through multiple chats. The sender should confirm the stablecoin and network, then send a small amount, such as $5 or $10.

Once the recipient confirms it arrived, both sides should check what happens next. Can the recipient hold it safely? Can they send it again if needed? Can they convert or spend it through a route that works in their country?

Only after that test should the sender consider sending a larger amount.

This is the right moment to try walllet.com with a small stablecoin receive. Download walllet.com, test the route with a small amount, and make sure both sides understand the flow before using it for regular family transfers.

When stablecoin remittances may not be the right choice

Stablecoins are not always better.

They may not be right if the recipient needs cash immediately and has no reliable cash-out route. They may not be right if the sender or recipient cannot confidently check networks and addresses. They may not be right if local rules restrict certain crypto activity. They may not be right if the family would treat the wallet like a bank account without understanding self-custody.

Here is the honest tradeoff: stablecoins can reduce friction, but they also move responsibility closer to the user.

That is powerful for people who want control. It is risky for people who are not ready for the basics.

The safest route is the one your family understands

The future of remittances will be won by money movement that families can understand.

For migrant workers, stablecoins can be useful when the full route is clear: how the sender gets the stablecoin, how the family receives it, which network is used, what the wallet shows, and how the recipient can use or convert the funds afterward.

Start small. Test the route. Teach the family what each step means. The best remittance setup is not the most advanced one. It is the one that still works when someone is tired, busy, and sending money because home needs it.

Ready to test stablecoin transfers with less wallet stress?

Download walllet.com and try receiving a small amount of USDT or USDC first. Start with a test transfer, confirm the network, make sure the recipient understands what arrived, and only then use it for regular family money movement.